Can't Afford a Home on Your Own? Some First-Time Buyers Are Solving That by Going in Together.

The desire to own a home hasn't gone anywhere. But for a growing number of first-time buyers, the math just isn't cooperating.

And some of them are getting creative about it.

The Dream Is Intact. The Affordability Gap Is Real.

According to FirstHome IQ, homeownership still ranks among the top life goals for the next generation. Young buyers haven't given up on it — not even close.

But 73% of Gen Z and millennial buyers cite affordability as the primary reason they haven't made homeownership a priority yet. And it's showing up in the data. First-time buyers now make up just 21% of all home purchases — the lowest share the National Association of Realtors has recorded since they started tracking it in 1981.

That's not a motivation problem. That's a math problem. And some buyers are solving it by changing the math entirely.

What Co-Buying Actually Is

Co-buying means purchasing a home with someone you're not married to — a friend, a sibling, an unmarried partner, even a trusted coworker. You combine incomes, split the down payment, and share the monthly costs.

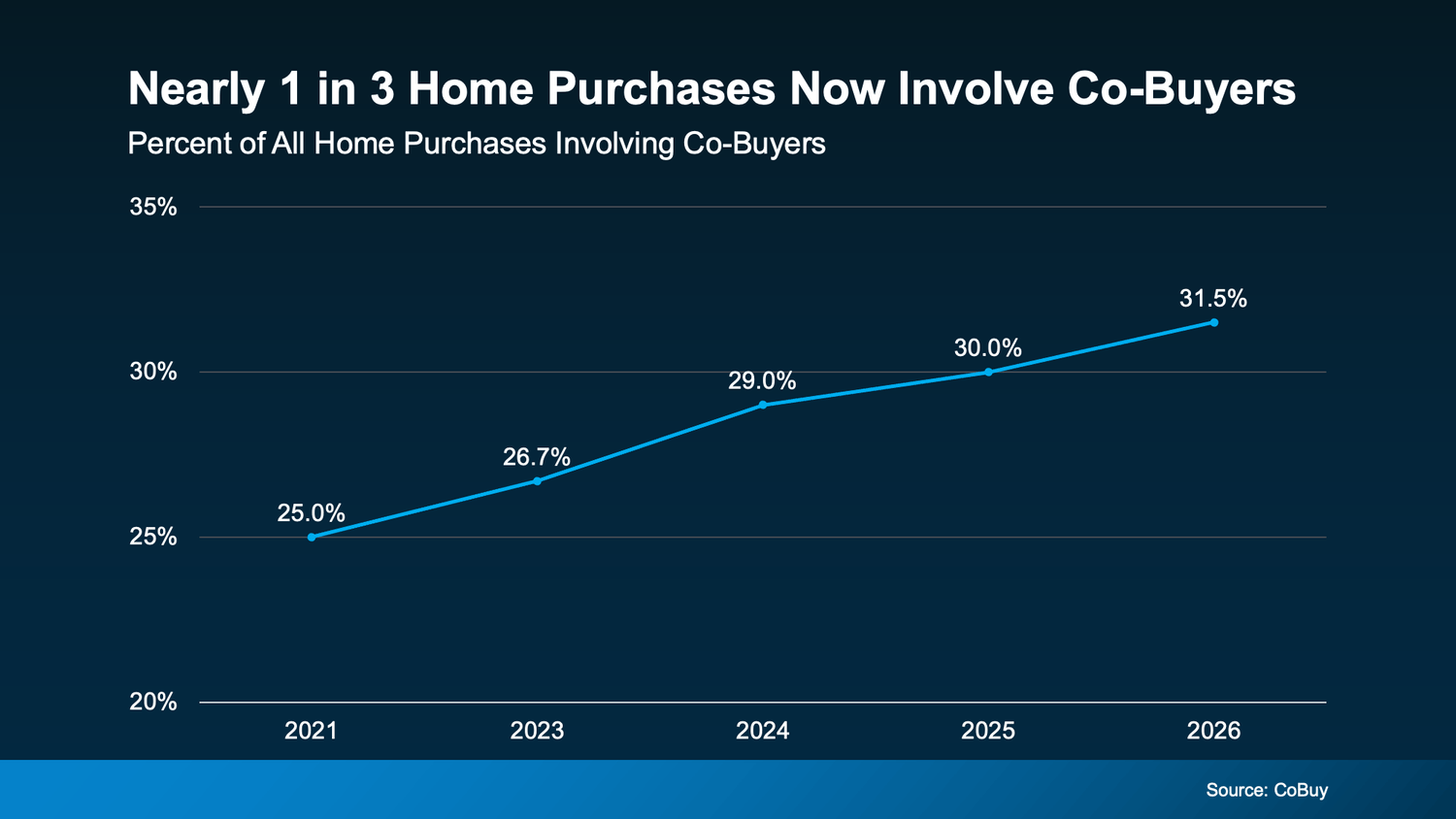

It's not a new concept, but it's gaining serious traction. According to CoBuy.io, 64 million Americans currently co-own a home with someone they're not married to. And 31.5% of home purchases today involve co-buyers.

That's not a fringe strategy. That's nearly one in three home purchases. And it's happening because for a lot of buyers, especially in higher-cost markets like Southern California, it's one of the most practical paths to ownership available right now.

Why It Works — Especially in SoCal

Here's what co-buying actually changes for buyers in Rancho Cucamonga, Pasadena, and across LA County and the Inland Empire:

It gets you there faster. Two people saving toward a down payment reach the goal significantly faster than one. In a market where time spent waiting is time spent building someone else's equity through rent, that acceleration matters.

It expands what you can afford. Combined incomes mean combined purchasing power. In Southern California, where even entry-level homes in desirable areas push $500,000–$600,000, that difference can be the line between qualifying for a home you actually want to live in versus one you're settling for.

It makes loan qualification easier. Lenders look at debt-to-income ratio (DTI) across all borrowers on the loan. More income means more borrowing power — and for buyers who are individually right on the edge of qualifying, adding a co-buyer can change the outcome entirely.

It reduces monthly costs. When two people split the mortgage, taxes, insurance, and maintenance, the monthly cost of owning can actually come out comparable to — or even less than — renting separately. In a market where rents have been climbing with no equity to show for it, that comparison deserves a hard look.

The Part You Have to Get Right

Co-buying works best when everyone goes in with eyes wide open — and a plan for the scenarios that feel unlikely until they aren't.

What happens if one person wants to sell and the other doesn't? What if one person loses their job and can't cover their share of the mortgage for a few months? How are costs split when something major needs to be repaired?

These aren't reasons to avoid co-buying. They're reasons to have the conversation before you close — and to put the answers in writing.

A co-ownership agreement isn't just a legal formality. It's a game plan for your investment. It keeps everyone aligned when things go smoothly — and protected if they don't. An attorney who handles real estate can help you draft one that covers the key scenarios specific to your arrangement.

The co-buying relationships that work well are built on trust, shared financial values, and clear communication from the start. If you have that foundation, the rest is logistics.

What This Looks Like in the Southern California Market

In Rancho Cucamonga, two buyers combining incomes might qualify for a newer townhome or single-family home that would be out of reach for either person individually — and start building equity in one of the Inland Empire's most sought-after communities.

In Pasadena, where prices are higher and the homes more established, co-buying with a sibling or close friend might be what finally makes that market accessible — splitting a mortgage on a character home that's appreciating in a market with strong long-term fundamentals.

The strategy isn't for everyone. But for the right buyers with the right relationship and the right planning, it's a legitimate and increasingly common path to ownership in a market that can feel otherwise impossible to crack.

Bold LA Key Takeaway

Affordability challenges are real — but they don't have to mean waiting indefinitely. Co-buying is helping first-time buyers stop renting and start building equity by changing the one variable they actually have control over: who they buy with.

If you're curious whether co-buying could work for your situation — what it would look like, what to watch out for, and what's available in your target market — let's talk it through.

There's more than one path to homeownership. Let's find the one that works for you.

That wraps up today's blog — appreciate you stopping by. And as always, if you want it to sell, call Terrell… and if you want to buy, I'm still the guy.

Terrell Bolden

REALTOR®

DRE#02110062

Realty Connection Group

Los Angeles, California

(323) 471-5295

Terrell Bolden has always had a passion for real estate and how it can be used as a tool to enhance daily life.

-A safe place to call home and raise a family.

-An appreciating asset that can be passed to loved ones, or used to finance the vacation of your dreams.

Terrell understands that real estate opportunities are plentiful and is deeply committed to helping others achieve their real estate dreams throughout the greater Los Angeles area.

Disclaimer: The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. Terrell Bolden, Realty Connection Group, DRE #02110062 does not guarantee or warrant the accuracy or completeness of the information or opinions contained herein. Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision. Terrell Bolden, Realty Connection Group, DRE #02110062 will not be liable for any loss or damage caused by your reliance on the information or opinions contained herein.

Let us know what you think in the comments!

Quick links

Newsletter

Subscribe to the newsletter and stay in the loop! By joining, you acknowledge that you'll receive our newsletter and can opt-out anytime hassle-free.