Foreclosure Headlines Are Back. Here's Why This Isn't 2008.

The word "foreclosure" has a way of stopping people mid-scroll. And if you've been seeing headlines about rising foreclosure activity lately, it's completely understandable if your mind went straight to 2008.

But before that anxiety takes hold, let's look at what the data actually shows — because the full picture is very different from what the headlines suggest.

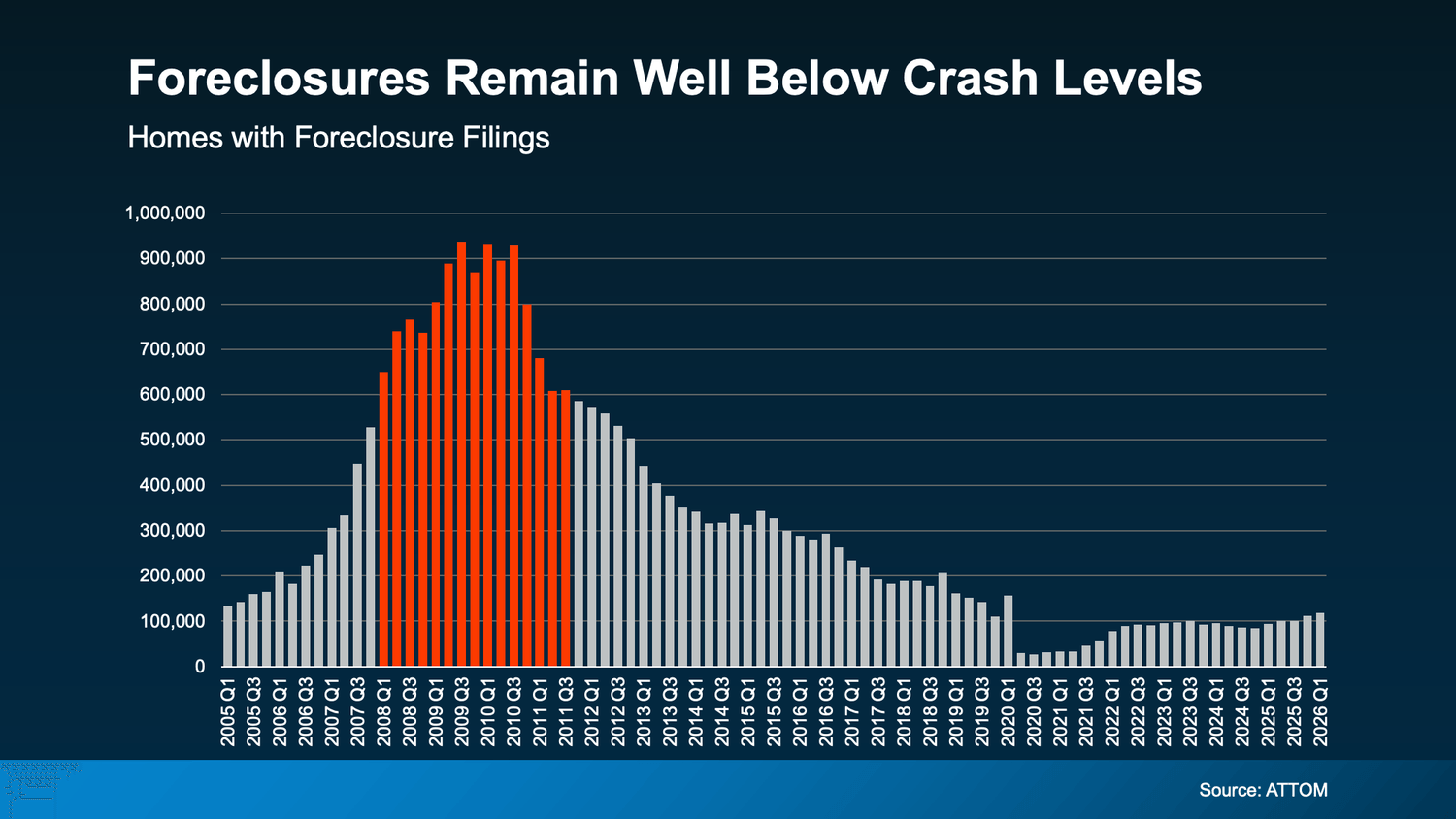

Yes, Foreclosures Are Up. Here's What That Number Actually Means.

According to ATTOM, foreclosure filings are up 26% from a year ago and have been rising for five straight quarters. That's a real trend — and it's worth acknowledging honestly.

But here's the context that changes everything:

The numbers that look "low" in 2020 and 2021 aren't the baseline. That's when the federal government implemented a foreclosure moratorium to protect homeowners during the pandemic. Those years were an exception — not the standard against which we should be measuring today.

The right comparison is 2017, 2018, and 2019 — the last years the housing market was operating normally. And when you stack today's numbers against those years, we're actually still below pre-pandemic norms.

Let that sink in. Despite five quarters of rising filings, we haven't even returned to what was considered a normal foreclosure environment before the pandemic. And we're nowhere near the levels of 2008. This is a market normalizing — not a market in crisis.

Why Today's Situation Is Fundamentally Different From 2008

The most important difference between now and 2008 comes down to one word: equity.

According to Cotality, the average homeowner today is sitting on approximately $295,000 in home equity. That number changes everything about what happens when a homeowner faces financial hardship.

In 2008, the crisis was devastating in large part because millions of homeowners were underwater — they owed more than their homes were worth. Selling wasn't an option. Walking away or losing the home to foreclosure was often the only door available.

That's not the situation today. A homeowner with substantial equity who hits a rough patch has real choices. They can sell, pay off their mortgage, cover the cost of the transaction, protect their credit, and potentially walk away with money in their pocket. That's a completely different outcome — and it's a major reason why today's rising filings are unlikely to spiral the way they did during the last crisis.

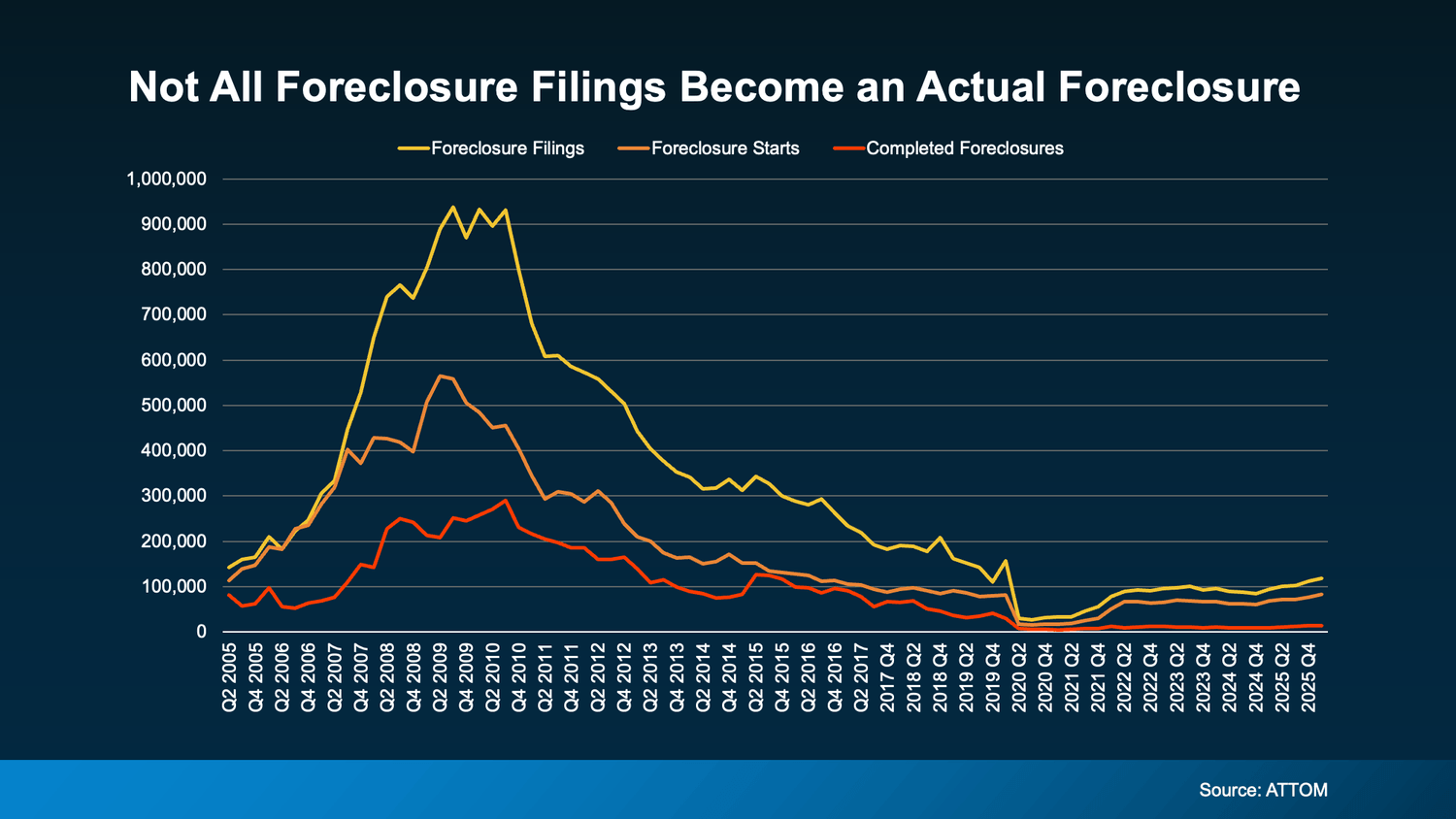

The Gap Between Filed and Foreclosed

Here's something the headlines never explain — and it matters a lot.

Look at that red line — completed foreclosures, meaning homes that were actually lost. It stays well below both the filings and the starts throughout the entire chart.

That gap tells the real story. A large percentage of homeowners who enter the foreclosure process never end up losing their home — because they find another path forward before it reaches that point. They work out a repayment plan with their lender. They sell. They refinance. They find a solution.

Today's equity levels are a big reason that gap exists and persists. And it's why the rising filing numbers you're seeing in the headlines don't translate directly into a wave of distressed homes flooding the market.

If You're Struggling, You Have More Options Than You Think

Maybe this article hit close to home because you're behind on payments and feeling the weight of that. If that's where you are, here's what I want you to know:

Missing a payment or two does not automatically mean you're going to lose your home. Banks would genuinely rather work with you than foreclose. Foreclosure is a complicated, expensive, time-consuming process for lenders — it's not their preferred outcome either.

If you're struggling, reach out to your lender sooner rather than later. The earlier you make that call, the more options you have. Lenders can often offer:

Repayment plans to catch up over time

Forbearance — a temporary pause or reduction in payments

Loan modifications that restructure your terms to be more manageable long-term

And if selling makes more sense for your situation — especially if you have equity — that's a conversation worth having with a real estate agent before the foreclosure process moves further along. Understanding what your home is worth and what you'd walk away with could completely change your options.

In some states, the foreclosure process moves faster than people expect. Getting ahead of it early gives you and your lender the most room to find a solution that works for everyone.

What This Means for Buyers and Sellers in Southern California

For buyers hoping that a flood of discounted foreclosure properties is coming — the data doesn't support that scenario. Most homeowners facing hardship today have enough equity to sell rather than foreclose, which means distressed inventory is unlikely to materialize at meaningful scale.

For sellers concerned about foreclosures dragging down neighborhood values — the same equity cushion that prevents mass foreclosures also prevents the kind of fire-sale pricing that characterized 2008.

The Southern California market — including Pasadena, Rancho Cucamonga, and the broader LA County and Inland Empire areas — is operating from a fundamentally stronger foundation than it was during the last crisis. Stricter lending standards, substantial homeowner equity, and a structural undersupply of housing all point in a different direction than 2008.

Bold LA Key Takeaway

Foreclosure activity is rising — but it's rising toward normal, not toward crisis. The equity most homeowners are sitting on today is the single biggest reason this looks nothing like 2008 — and why most of the filings you're reading about won't result in a homeowner actually losing their property.

Don't let alarming headlines drive decisions about one of the biggest financial assets in your life. Context matters. And the context here is actually reassuring.

If you have questions about what's happening in the market — or if you're in a tough spot and want to understand your options — reach out. That's exactly the kind of conversation I'm here for.

That wraps up today's blog — appreciate you stopping by. And as always, if you want it to sell, call Terrell… and if you want to buy, I'm still the guy.

Terrell Bolden

REALTOR®

DRE#02110062

Realty Connection Group

Los Angeles, California

(323) 471-5295

Terrell Bolden has always had a passion for real estate and how it can be used as a tool to enhance daily life.

-A safe place to call home and raise a family.

-An appreciating asset that can be passed to loved ones, or used to finance the vacation of your dreams.

Terrell understands that real estate opportunities are plentiful and is deeply committed to helping others achieve their real estate dreams throughout the greater Los Angeles area.

Disclaimer: The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. Terrell Bolden, Realty Connection Group, DRE #02110062 does not guarantee or warrant the accuracy or completeness of the information or opinions contained herein. Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision. Terrell Bolden, Realty Connection Group, DRE #02110062 will not be liable for any loss or damage caused by your reliance on the information or opinions contained herein.

Let us know what you think in the comments!

Quick links

Newsletter

Subscribe to the newsletter and stay in the loop! By joining, you acknowledge that you'll receive our newsletter and can opt-out anytime hassle-free.