Home Insurance Costs Are Rising. Here's What Every Buyer Needs to Know Before They Close.

When most buyers think about the cost of homeownership, they focus on two numbers: the purchase price and the mortgage payment. But there's a third cost that's been quietly climbing — and if you're not planning for it upfront, it can catch you off guard after you've already closed.

Home insurance premiums are going up. And in certain markets, including parts of Southern California, the increase is significant enough to meaningfully affect your monthly budget.

Here's what's driving it, what to expect, and how to plan around it.

First, Let's Be Clear About What You're Actually Paying For

Home insurance isn't optional — most lenders require it. And understanding what it covers helps explain why it matters so much:

Repairs and rebuilding costs — if your home is damaged by fire, a storm, or another covered event, your policy helps cover the cost to repair or fully rebuild

Personal belongings — furniture, electronics, clothing, jewelry — covered if stolen or damaged in a covered event

Liability protection — if someone is injured on your property, your policy can help cover medical bills or legal expenses

It's the safety net protecting what is likely the largest purchase of your life. The question isn't whether you need it — it's how to budget for what it costs right now.

Why Premiums Have Been Climbing

The root causes aren't complicated, even if the insurance industry likes to make them sound that way.

According to the Insurance Research Council, two things are happening simultaneously: severe weather events and natural disasters are occurring more frequently — generating more claims — and the cost of building materials and labor has gone up significantly, meaning those claims cost more to resolve.

More claims plus higher repair costs equals higher premiums. That's the math.

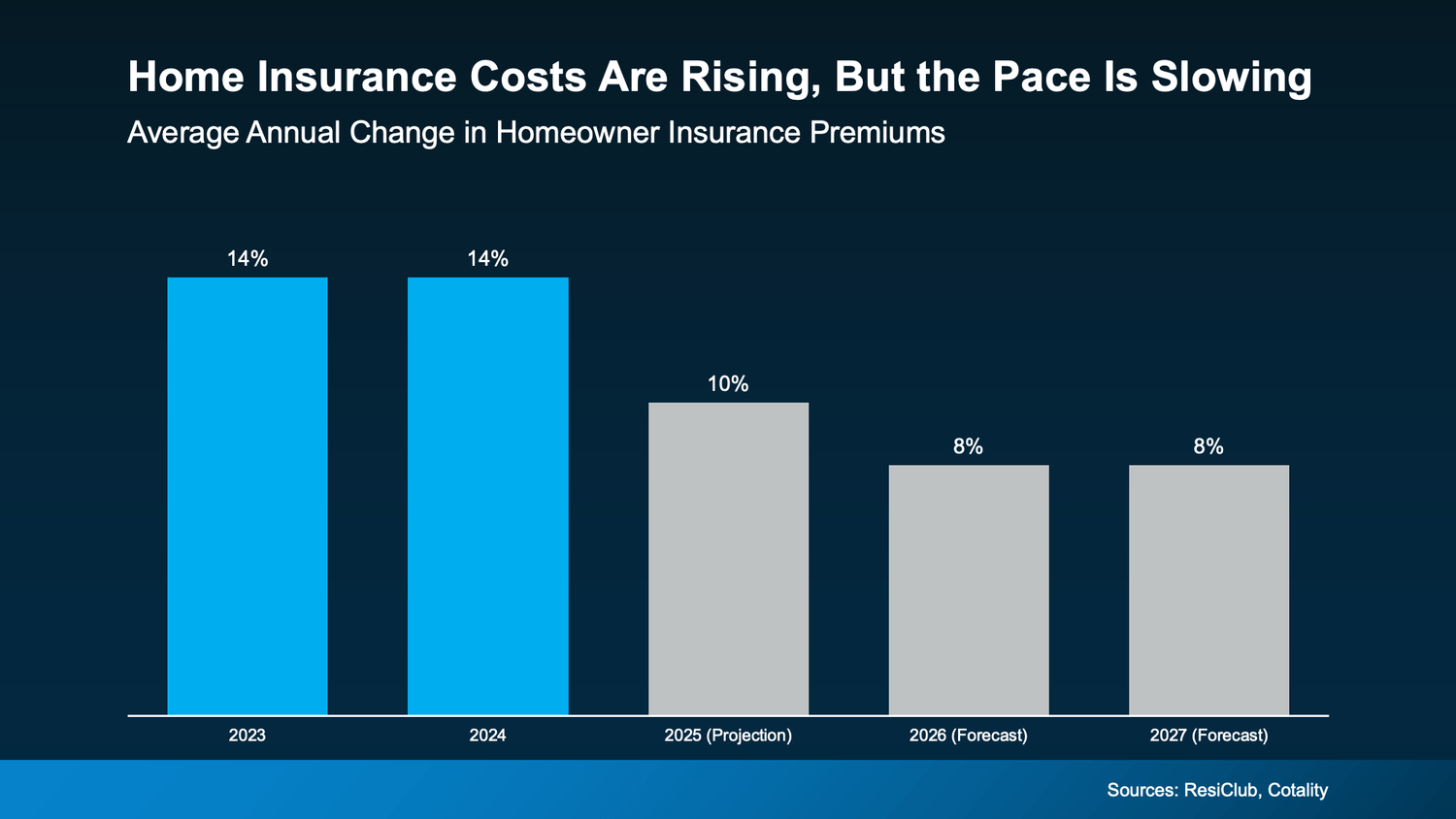

Here's the slightly better news: the pace of those increases is expected to slow.

2023 and 2024: premiums rose about 14% per year

2025: the increase slowed to about 10%

2026 and 2027: projected increases of around 8% per year

Still going up — but decelerating. That's a meaningful distinction for buyers trying to plan their long-term housing budget.

The Silver Lining Buyers Should Know About

Here's something worth keeping in mind as you factor insurance costs into your budget: while insurance is going up, mortgage rates have come down. And that offset matters.

As Michael Gaines, Senior VP of Capital Markets at Cardinal Financial, explains, rising taxes and insurance create pressure — but they don't erase the benefits of a lower rate. A small rate improvement, paired with the right loan program and smart planning, can still make homeownership work. It's about layering the right solutions together, not looking at any one cost in isolation.

In other words: don't let rising insurance costs become the reason you dismiss homeownership entirely. Look at the full picture — including what lower rates are doing for your monthly payment on the other side of the ledger.

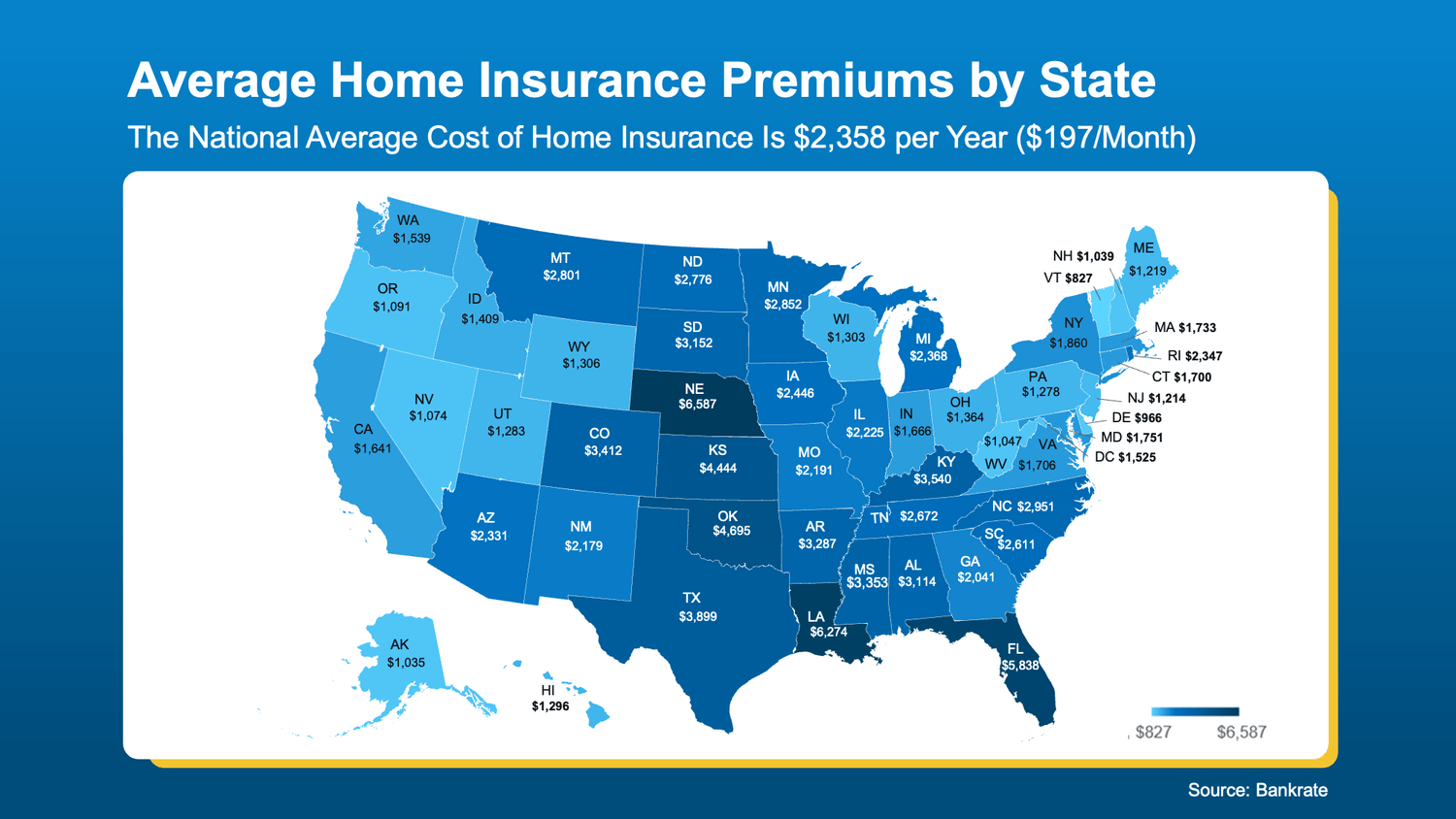

What You Should Budget — And Why It Depends on Where You Buy

Insurance costs aren't the same everywhere. They vary based on location, the home's age and construction, proximity to fire zones or flood plains, coverage level, and more.

In Southern California, this conversation requires particular honesty. LA County and surrounding areas have seen some of the most significant insurance market challenges in the country in recent years. Wildfire risk has caused several major insurers to reduce or eliminate coverage in certain zip codes — which means buyers in affected areas may face higher premiums, limited carrier options, or the need to explore California's FAIR Plan as a coverage option.

This isn't meant to alarm — it's meant to prepare you. Because buyers who factor insurance costs in before making an offer are in a much stronger position than those who discover the issue after they're already under contract.

In Rancho Cucamonga and the Inland Empire, insurance costs are generally more manageable than in high-fire-risk areas of LA County — but they've still trended upward along with the rest of the state. Getting insurance quotes before you're under contract on a specific property is a smart move regardless of where you're looking.

What Smart Buyers Are Doing Right Now

Here's the practical guidance I give every buyer I work with in this market:

Get insurance quotes early — before you're under contract. Don't wait until after your offer is accepted to find out what coverage will actually cost on that specific property. In some cases, the insurance picture can meaningfully change the math on whether a home makes financial sense.

Ask your lender to factor insurance into your full payment estimate. Your mortgage payment is principal, interest, taxes, and insurance — all four. Make sure the number you're qualifying against reflects the real cost, not a placeholder.

Shop multiple carriers. Insurance rates vary significantly between providers, especially in California's evolving market. A good insurance broker who knows the local landscape can make a real difference in what you pay.

Don't let it derail you — plan around it. Rising insurance costs are a real factor, but they're a manageable one when you know about them upfront. Buyers who do this homework before they're emotionally committed to a specific home make much clearer, more confident decisions.

BOLD LA KEY TAKEAWAY

Home insurance is a real and rising cost of homeownership — and in Southern California, it deserves more attention in the planning process than most buyers give it. But it's not a reason to stay on the sidelines. It's a reason to plan smarter.

Know what coverage will cost on a property before you fall in love with it. Factor it into your full monthly payment calculation. And work with people who can help you navigate the options.

If you want to talk through what homeownership actually costs in the areas you're considering — including insurance — let's have that conversation before you're under contract. That's exactly when it's most useful.

Terrell Bolden

REALTOR®

DRE#02110062

Realty Connection Group

Los Angeles, California

(323) 471-5295

Terrell Bolden has always had a passion for real estate and how it can be used as a tool to enhance daily life.

-A safe place to call home and raise a family.

-An appreciating asset that can be passed to loved ones, or used to finance the vacation of your dreams.

Terrell understands that real estate opportunities are plentiful and is deeply committed to helping others achieve their real estate dreams throughout the greater Los Angeles area.

Disclaimer: The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. Terrell Bolden, Realty Connection Group, DRE #02110062 does not guarantee or warrant the accuracy or completeness of the information or opinions contained herein. Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision. Terrell Bolden, Realty Connection Group, DRE #02110062 will not be liable for any loss or damage caused by your reliance on the information or opinions contained herein.

Let us know what you think in the comments!

Quick links

Newsletter

Subscribe to the newsletter and stay in the loop! By joining, you acknowledge that you'll receive our newsletter and can opt-out anytime hassle-free.