Your Home Equity Could Be the Reason Someone You Love Gets to Buy Their First Home

If you've watched a son, daughter, or grandchild struggle to break into the housing market lately, you already know how frustrating it is to witness from the outside.

You know what homeownership did for your life. The stability it created. The wealth it helped you build over time. And you want that for them — but the path to get there feels a lot harder than it was when you bought your first home.

Here's something worth considering: the equity sitting in your home right now might be exactly what bridges that gap.

What You've Built Without Fully Realizing It

If you've owned your home for ten, twenty, or thirty-plus years, two things have been quietly working in your favor the entire time:

Your home's value went up. And your mortgage balance went down — or maybe you paid it off entirely.

That combination has created significant equity for a lot of long-term homeowners. And while most people think of that equity as something to access in retirement, it can serve another powerful purpose right now: helping the next generation clear the biggest obstacle standing between them and homeownership.

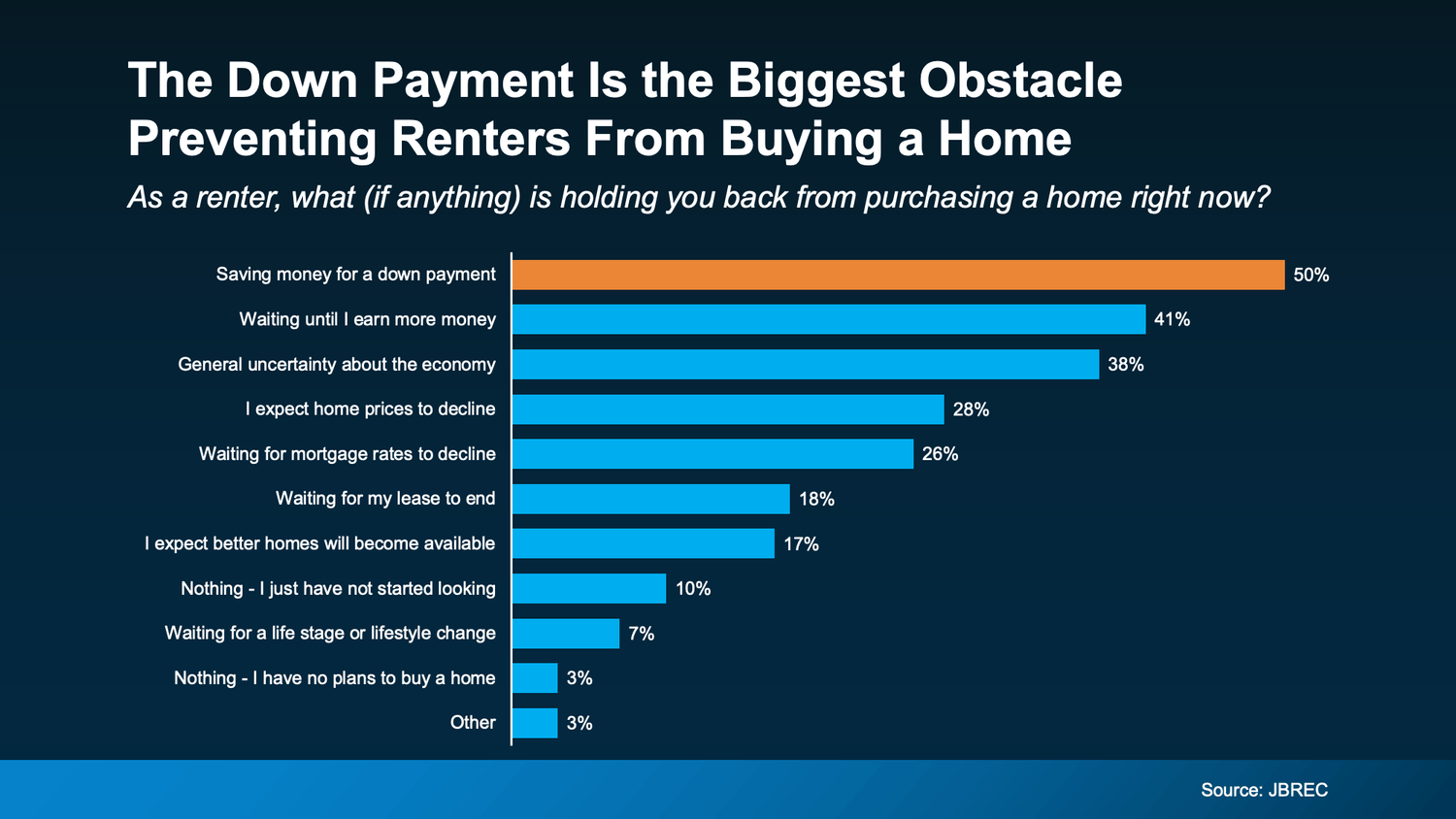

The #1 Thing Actually Holding Young Buyers Back

When John Burns Research & Consulting asked renters what was keeping them from buying, the answer wasn't mortgage rates. It wasn't home prices.

It was the upfront cost — specifically, saving enough for a down payment.

That's the wall. And for a lot of young buyers in Southern California — where even entry-level homes in markets like Rancho Cucamonga require a meaningful down payment, and Pasadena sits at an even higher price point — that wall feels nearly impossible to scale on their own.

You can't control mortgage rates. You can't control home prices. But you may be able to help with that upfront cost in a way that genuinely changes someone's trajectory.

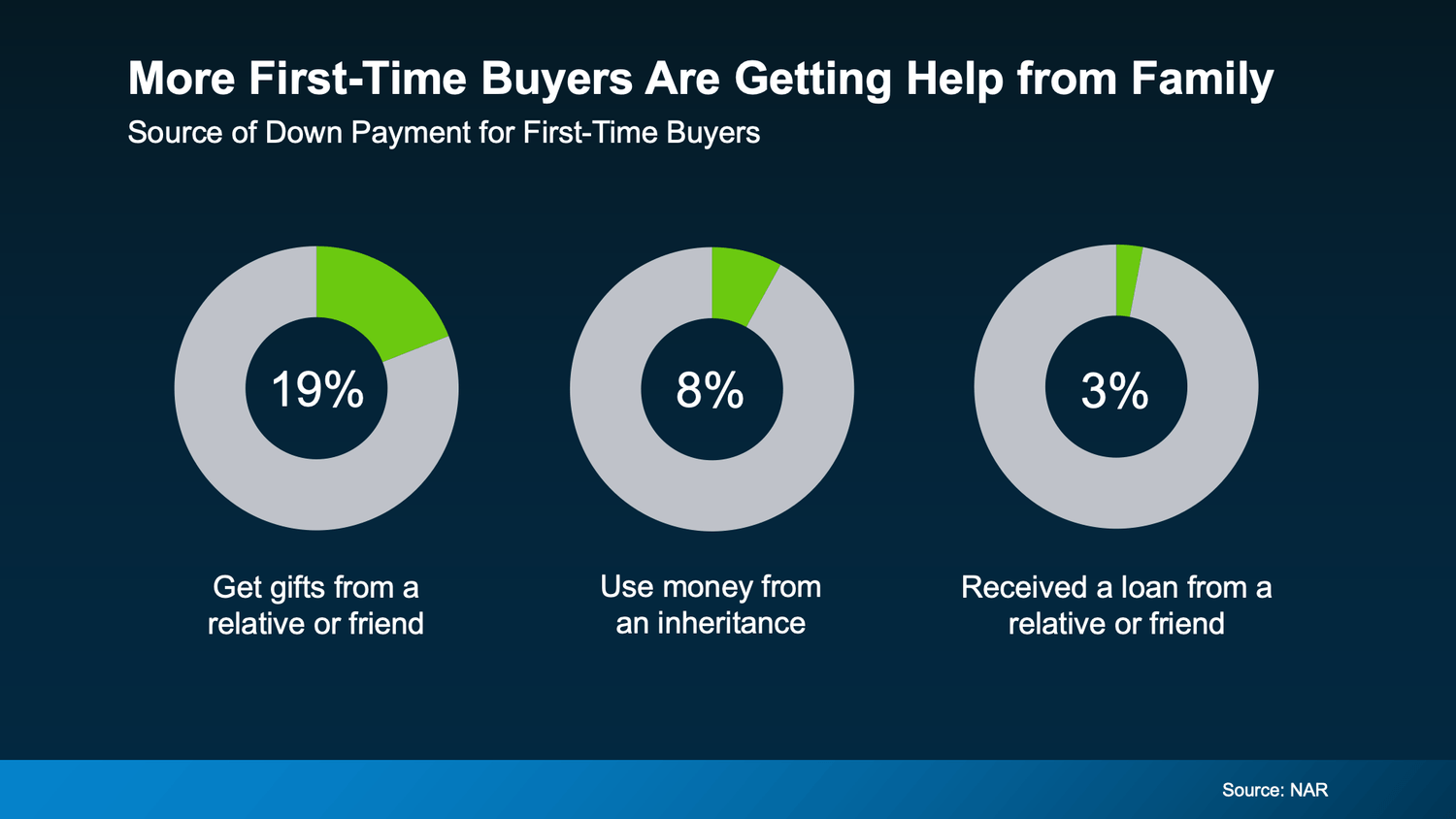

Help From Family Is Already Making It Happen

This isn't a fringe strategy. It's already happening at scale.

According to the National Association of Realtors, nearly 1 in 5 first-time buyers uses a cash gift from a family member or loved one toward their down payment. And beyond outright gifts, other young buyers are using inheritances or family loans to finally break into the market.

With an estimated $68 to $84 trillion of wealth expected to transfer from older generations to younger ones over the next two decades, a lot of families are rethinking the traditional approach of "passing it down eventually." Some are asking a different question: what if the most impactful time to help is now — when it actually changes what's possible for them?

What This Could Look Like in Practice

Let's say you've owned your home in the Inland Empire for 15 years. Depending on when you bought and what you owe, you might be sitting on $300,000, $400,000, or more in equity. Even accessing a fraction of that — through a cash-out refinance or a HELOC — could provide enough for a family member's down payment and closing costs without meaningfully disrupting your own retirement plans.

And here's the part that matters most: a down payment gift doesn't just help someone buy a house. It starts a wealth-building cycle for the next generation. Equity. Appreciation. Stability. The exact things that changed your financial life — they get to experience too.

In Rancho Cucamonga, a 3.5% FHA down payment on a $550,000 home is about $19,000. In Pasadena, a conventional purchase might require more. But either way, a meaningful contribution from a parent or grandparent who has equity to work with can be the difference between "someday" and "next year."

This Is About Opportunity, Not Obligation

I want to be clear about something. This isn't a suggestion that every homeowner should tap their equity for their kids or grandkids. Every family's financial situation is different — and your own security has to come first.

But if you've built substantial equity over the years and you've been watching a loved one struggle to break into the market, it's worth at least understanding what's possible. You may have more room to help than you think — and still have plenty left for the retirement you've planned.

The question isn't whether you should do it. The question is whether you've actually looked at the numbers to know what your options are.

Bold LA Key Takeaway

Homeownership changed your life. Your equity might be the thing that changes theirs.

If you're curious what your current equity position looks like — and what it could realistically make possible for you or someone you love — let's start with a simple conversation. I'll help you understand what you're working with and what options exist, so you can make the best decision for your family.

Sometimes the most powerful investment you can make isn't in the market. It's in the next generation.

Terrell Bolden

REALTOR®

DRE#02110062

Realty Connection Group

Los Angeles, California

(323) 471-5295

Terrell Bolden has always had a passion for real estate and how it can be used as a tool to enhance daily life.

-A safe place to call home and raise a family.

-An appreciating asset that can be passed to loved ones, or used to finance the vacation of your dreams.

Terrell understands that real estate opportunities are plentiful and is deeply committed to helping others achieve their real estate dreams throughout the greater Los Angeles area.

Disclaimer: The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. Terrell Bolden, Realty Connection Group, DRE #02110062 does not guarantee or warrant the accuracy or completeness of the information or opinions contained herein. Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision. Terrell Bolden, Realty Connection Group, DRE #02110062 will not be liable for any loss or damage caused by your reliance on the information or opinions contained herein.

Let us know what you think in the comments!

Quick links

Newsletter

Subscribe to the newsletter and stay in the loop! By joining, you acknowledge that you'll receive our newsletter and can opt-out anytime hassle-free.