If You're a Veteran and Think Homeownership Is Out of Reach — Read This First.

Nearly half of all Veterans — 49% — believe homeownership is currently out of reach for them, according to a recent NewDay USA survey.

And that number bothers me. Because a lot of those Veterans are closer to buying than they realize. They just don't have the full picture of what their VA loan benefit actually covers.

If you've served — or you know someone who has — this one's worth reading carefully.

The Benefit Has Been Around for 80+ Years. The Misconceptions Have Too.

The VA home loan benefit isn't new. It's been around for over eight decades. But knowing it exists and understanding what it actually does are two very different things.

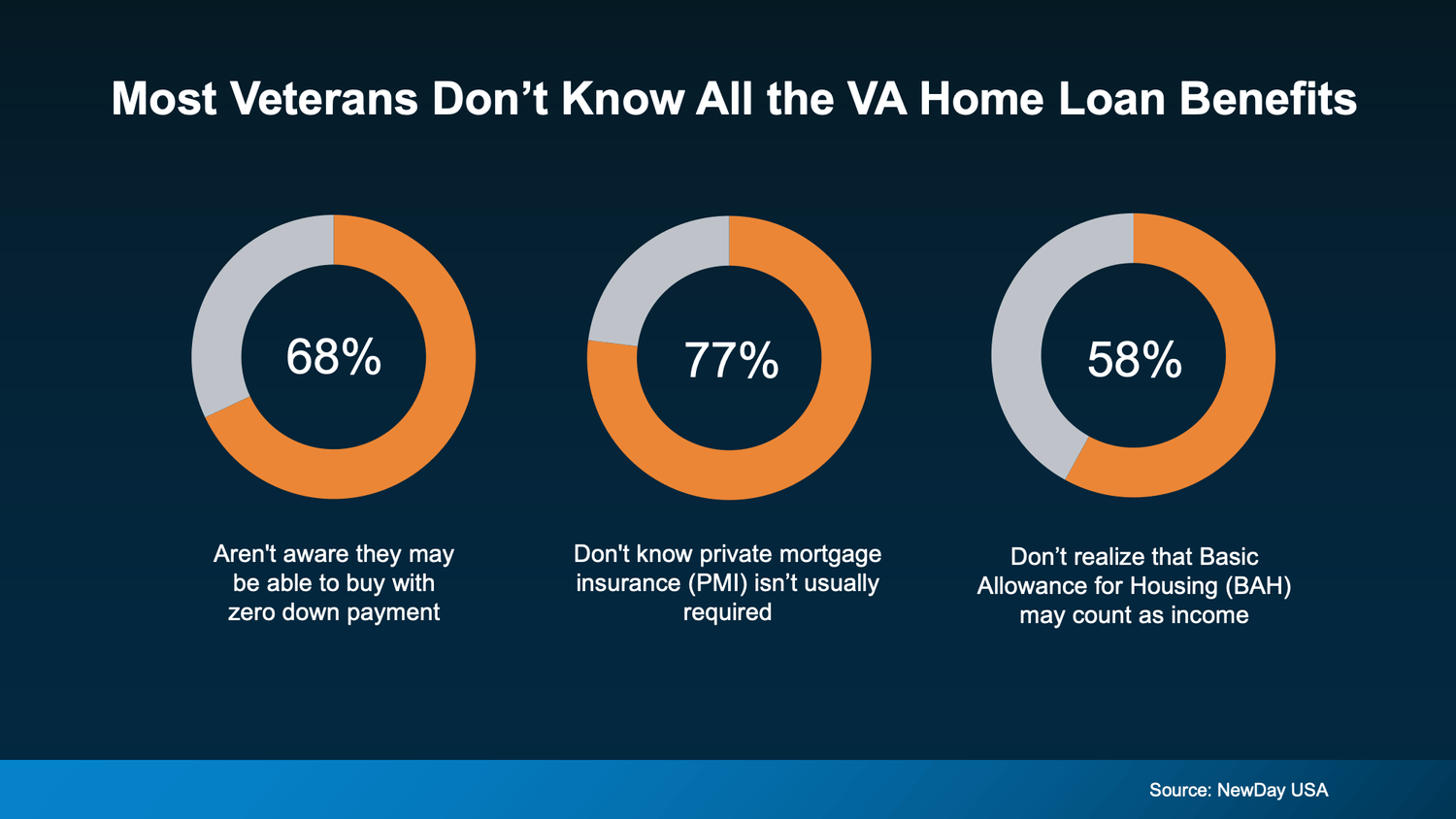

Three misconceptions consistently trip Veterans up — and any one of them could be the reason someone who qualifies isn't buying:

Let's walk through all three — because the reality is significantly better than what most Veterans assume.

Misconception #1: You Need a Large Down Payment

This is the biggest one — and it's keeping a lot of Veterans on the sidelines unnecessarily.

According to the NewDay USA survey, many Veterans assumed they'd need to save somewhere between $10,000 and $19,900 before they could buy. That's years of saving — for an upfront cost that often isn't required at all.

VA loans offer the ability to put zero money down for qualified buyers. Zero. That's not a teaser or a limited offer. It's one of the core benefits of the program — earned through service.

For a first-time buyer in Rancho Cucamonga looking at a $550,000 home, the difference between saving a 3.5% FHA down payment ($19,250) and a 0% VA down payment is significant. That gap in savings timeline could be the difference between buying this year and buying in three years.

Misconception #2: Closing Costs Are the Same as Any Other Loan

Closing costs catch a lot of buyers off guard — VA loan or not. But here's what's different: according to the Department of Veterans Affairs, VA loans come with limits on the types of closing costs buyers are required to pay.

That means more money stays in your pocket on closing day. And when you combine that with the zero-down-payment benefit, the total upfront cost of buying with a VA loan can be dramatically lower than Veterans expect — or than any comparable loan program offers.

Less to save. Faster path to buying. That's what this benefit is designed to do.

Misconception #3: You'll Still Pay PMI Without 20% Down

With most conventional loans, putting less than 20% down means paying private mortgage insurance — PMI — every single month until you hit that 20% equity threshold. According to NewDay USA, that typically runs $100 to $300 per month.

Over five years, that's potentially $18,000 in additional costs that build no equity and disappear the moment you hit the threshold.

VA loans don't require PMI. Even with zero down. That monthly savings is real money — money that could go toward building your life in that home instead of covering an insurance premium that only protects the lender.

One More Thing Active Duty Members Should Know

If you're currently on active duty or a qualifying reservist, your Basic Allowance for Housing (BAH) and Basic Allowance for Subsistence (BAS) may count toward income qualification on a VA loan.

Here's why that matters: both BAH and BAS are non-taxable income. When a lender factors them into your qualification, it can meaningfully increase the loan amount you're approved for — often more than Veterans expect when they're running the numbers without those allowances included.

If you've done a rough calculation of what you'd qualify for and left BAH or BAS out of the equation, run it again with a lender who understands VA loans. The answer might look very different.

What This Looks Like in Southern California

In Pasadena and LA County, where purchase prices are higher, the VA loan's zero-down and no-PMI combination carries even more weight. The monthly savings from avoiding PMI on a $700,000+ loan are substantial — and the elimination of a down payment requirement removes what is often the single biggest barrier to entry in that market.

In Rancho Cucamonga and the Inland Empire, the VA benefit opens doors to newer construction, larger floor plans, and family-friendly communities that might otherwise require years of additional saving to access. For Veterans and active duty families looking to put down roots in the IE, this benefit is one of the most powerful tools available.

Bold LA Key Takeaway

The VA home loan benefit is one of the most powerful homebuying tools available — and it's being underutilized because of misconceptions that simply aren't accurate.

No down payment required. Limited closing costs. No PMI. BAH and BAS counting toward qualification. For Veterans who've been running numbers that don't include these advantages, the real picture looks significantly better.

If you're a Veteran, active duty, or know someone who is — and homeownership feels out of reach — let's talk before you write it off. The math might surprise you.

I'll connect you with a lender who specializes in VA loans and make sure you have the full picture before you make any decisions.

That wraps up today's blog — appreciate you stopping by. And as always, if you want it to sell, call Terrell… and if you want to buy, I'm still the guy.

Terrell Bolden

REALTOR®

DRE#02110062

Realty Connection Group

Los Angeles, California

(323) 471-5295

Terrell Bolden has always had a passion for real estate and how it can be used as a tool to enhance daily life.

-A safe place to call home and raise a family.

-An appreciating asset that can be passed to loved ones, or used to finance the vacation of your dreams.

Terrell understands that real estate opportunities are plentiful and is deeply committed to helping others achieve their real estate dreams throughout the greater Los Angeles area.

Disclaimer: The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. Terrell Bolden, Realty Connection Group, DRE #02110062 does not guarantee or warrant the accuracy or completeness of the information or opinions contained herein. Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision. Terrell Bolden, Realty Connection Group, DRE #02110062 will not be liable for any loss or damage caused by your reliance on the information or opinions contained herein.

Let us know what you think in the comments!

Quick links

Newsletter

Subscribe to the newsletter and stay in the loop! By joining, you acknowledge that you'll receive our newsletter and can opt-out anytime hassle-free.