Inflation Is Moving in the Wrong Direction. Here's What That Actually Means for Your Move.

Let's talk about something that's affecting every buyer and seller right now — and that most people only half-understand because the headlines aren't explaining it clearly.

Inflation is back in the conversation. And if you're thinking about buying or selling a home, you need to know what's actually driving it, what it means for mortgage rates, and — most importantly — what you can do about it.

What's Actually Happening With Inflation Right Now

The government tracks inflation in several ways. One of the most closely watched is the PCE — the Personal Consumption Expenditures Price Index. It measures how much more people are paying for goods and services compared to a year ago.

And right now, it's moving in the wrong direction.

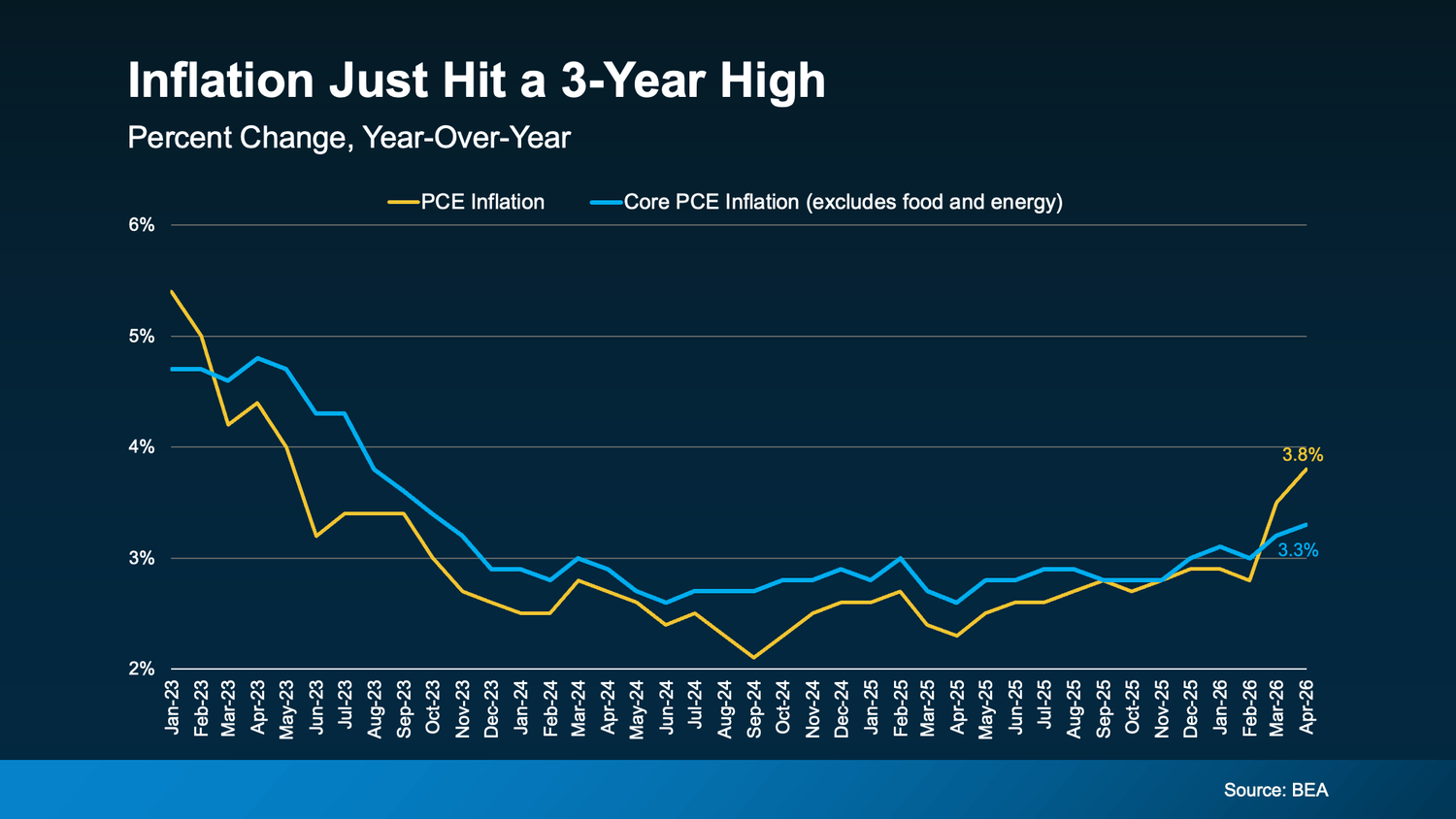

Here's what that chart is actually telling you — because there are two lines and the difference between them matters:

The yellow line is overall PCE — and yes, it's spiked sharply since February. A significant driver of that jump is the ongoing conflict in the Middle East, which has pushed gas and energy prices meaningfully higher. When you fill up your tank and wince at the number, that's what you're feeling.

The blue line is core PCE — the same measurement but with gas and energy prices removed. This is actually the number the Federal Reserve watches most closely, because energy prices are volatile and can skew the picture in both directions.

And here's the somewhat encouraging part: core PCE is rising — but nowhere near as fast as the headline number. That suggests a significant portion of the inflation spike we're seeing right now is directly tied to what's happening overseas. When that situation stabilizes, inflation may ease with it.

That's not a guarantee. But it's important context the headlines aren't giving you.

Why This Connects Directly to Your Mortgage Rate

Here's the housing link that matters most for buyers right now.

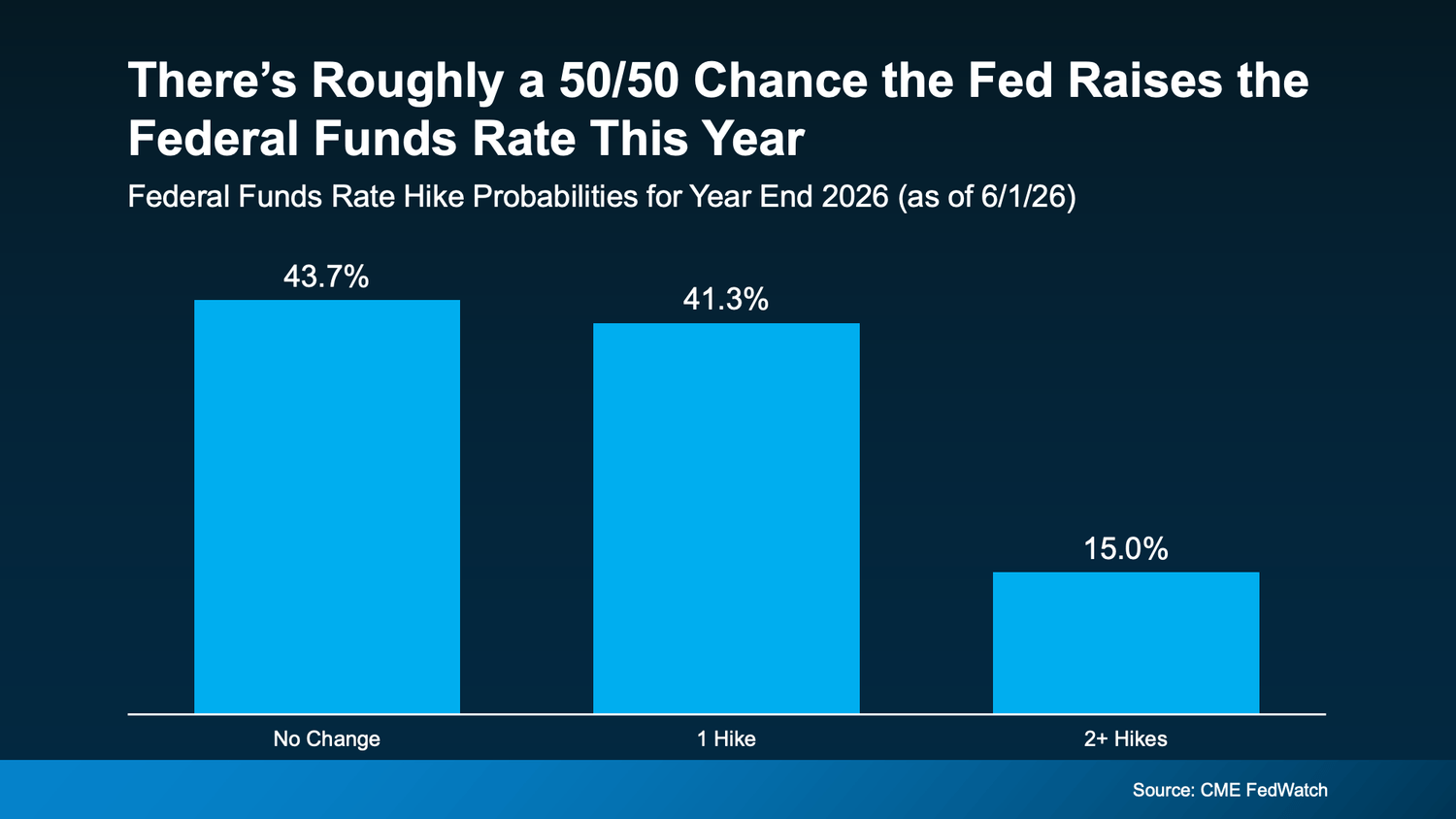

When inflation runs hot, the Federal Reserve tends to keep the Federal Funds Rate elevated — or raise it further — to cool spending and bring prices back under control. And while it's not a direct one-to-one relationship, the Fed's rate environment has real influence on where mortgage rates land.

Right now, according to CME FedWatch, there's roughly a 50/50 chance the Fed actually raises rates before the end of 2026:

That's not a certainty. But it's a real possibility — and it matters for anyone who's been sitting on the sidelines waiting for mortgage rates to drop significantly before making a move.

As Bankrate explains, oil prices and bond yields have pulled back slightly from their peaks — but they're still significantly elevated compared to the start of spring. Until there's a resolution to the conflict driving energy prices higher, both inflation and mortgage rates are likely to stay elevated.

"Higher for longer" isn't just a phrase anymore. It's the realistic scenario buyers and sellers need to plan around.

Before You Panic — This Is Not 2008

Every time inflation spikes or the economy gets uncomfortable, the same fear surfaces: "Is this going to be like 2008?"

It's not. And the reasons why matter:

Inventory is still relatively low nationally — there's no flood of distressed homes hitting the market looking for desperate buyers. Most homeowners today are sitting on substantial equity — the opposite of the underwater borrowers who triggered the last crisis. Lending standards are dramatically stricter than the anything-goes environment that preceded 2008. And today's challenge is affordability — which is real and hard — not a wave of foreclosures from borrowers who never should have qualified in the first place.

Uncomfortable and unhealthy are not the same thing. The market feels difficult right now. But difficult and crashing are very different situations — and confusing the two leads to bad decisions.

What This Means in Southern California Specifically

In Pasadena and LA County, the inflation and rate environment is adding pressure to a market that was already expensive. But the structural factors that have always supported values in that market — limited inventory, consistent demand, constrained supply — haven't changed. Sellers aren't panicking. They're adjusting expectations on timing.

In Rancho Cucamonga and the Inland Empire, buyers are feeling the rate pressure most acutely — especially first-time buyers who are working with tighter budgets. But this is also where the tools available to buyers matter most. Builder incentives, rate buydowns, down payment assistance programs, and seller concessions are all more accessible in this market than they were during the frenzy years. The path looks different than it did in 2021. It still exists.

What To Actually Do Right Now

High inflation and elevated rates don't mean homeownership is off the table. They mean the strategy looks different than it would in a lower-rate environment. Here's where to focus:

Talk to your lender about loan options that work in this environment. Adjustable-rate mortgages can offer meaningfully lower initial payments for buyers who have a clear timeline. Builder rate buydowns can permanently or temporarily reduce your rate. These aren't tricks — they're legitimate tools that change the monthly math in real ways.

Explore assistance programs you may not know about. California has active down payment assistance programs. Seller concessions are back on the table in many markets. First-time buyer programs exist specifically for this environment. Most buyers don't fully explore these options before assuming they can't afford to buy.

Stay ready to move when rates shift. The buyers who benefit most when rates ease aren't the ones who start their search at that moment. They're the ones who did the groundwork — pre-approved, clear on budget, connected with a trusted agent — so they can act quickly when the window opens. By the time rates drop and feel comfortable to everyone, the competition has already returned.

The right strategy, built around your specific situation, matters far more than waiting for a perfect market moment that may not come in the timeframe you're hoping for.

Bold LA Key Takeaway

Inflation is real. Rates are elevated. And the Fed might raise them further before this year is over. That's the honest picture.

But none of that means you're out of options. It means your strategy needs to be smarter — and your team needs to be better — than what would have been sufficient in a more forgiving market.

The buyers and sellers who navigate this environment successfully aren't the ones who waited for it to get easier. They're the ones who built a plan around where things actually are right now.

If you want to cut through the noise and figure out what this environment actually means for your specific situation — buying, selling, or just planning — let's talk. That conversation is exactly what I'm here for.

That wraps up today's blog — appreciate you stopping by. And as always, if you want it to sell, call Terrell… and if you want to buy, I'm still the guy.

Terrell Bolden

REALTOR®

DRE#02110062

Realty Connection Group

Los Angeles, California

(323) 471-5295

Terrell Bolden has always had a passion for real estate and how it can be used as a tool to enhance daily life.

-A safe place to call home and raise a family.

-An appreciating asset that can be passed to loved ones, or used to finance the vacation of your dreams.

Terrell understands that real estate opportunities are plentiful and is deeply committed to helping others achieve their real estate dreams throughout the greater Los Angeles area.

Disclaimer: The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. Terrell Bolden, Realty Connection Group, DRE #02110062 does not guarantee or warrant the accuracy or completeness of the information or opinions contained herein. Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision. Terrell Bolden, Realty Connection Group, DRE #02110062 will not be liable for any loss or damage caused by your reliance on the information or opinions contained herein.

Let us know what you think in the comments!

Quick links

Newsletter

Subscribe to the newsletter and stay in the loop! By joining, you acknowledge that you'll receive our newsletter and can opt-out anytime hassle-free.