Record Mortgage Debt Just Hit an All-Time High. Here's What That Headline Isn't Telling You.

You've probably seen the headline. Maybe your brother-in-law brought it up at dinner like he'd been saving it all week:

"Mortgage debt in America just hit a record high."

And here's the thing — he's not wrong. The number is real. But he only has half the story. And the half he's missing changes everything about what that headline actually means.

The Number Is Real. The Context Is What Matters.

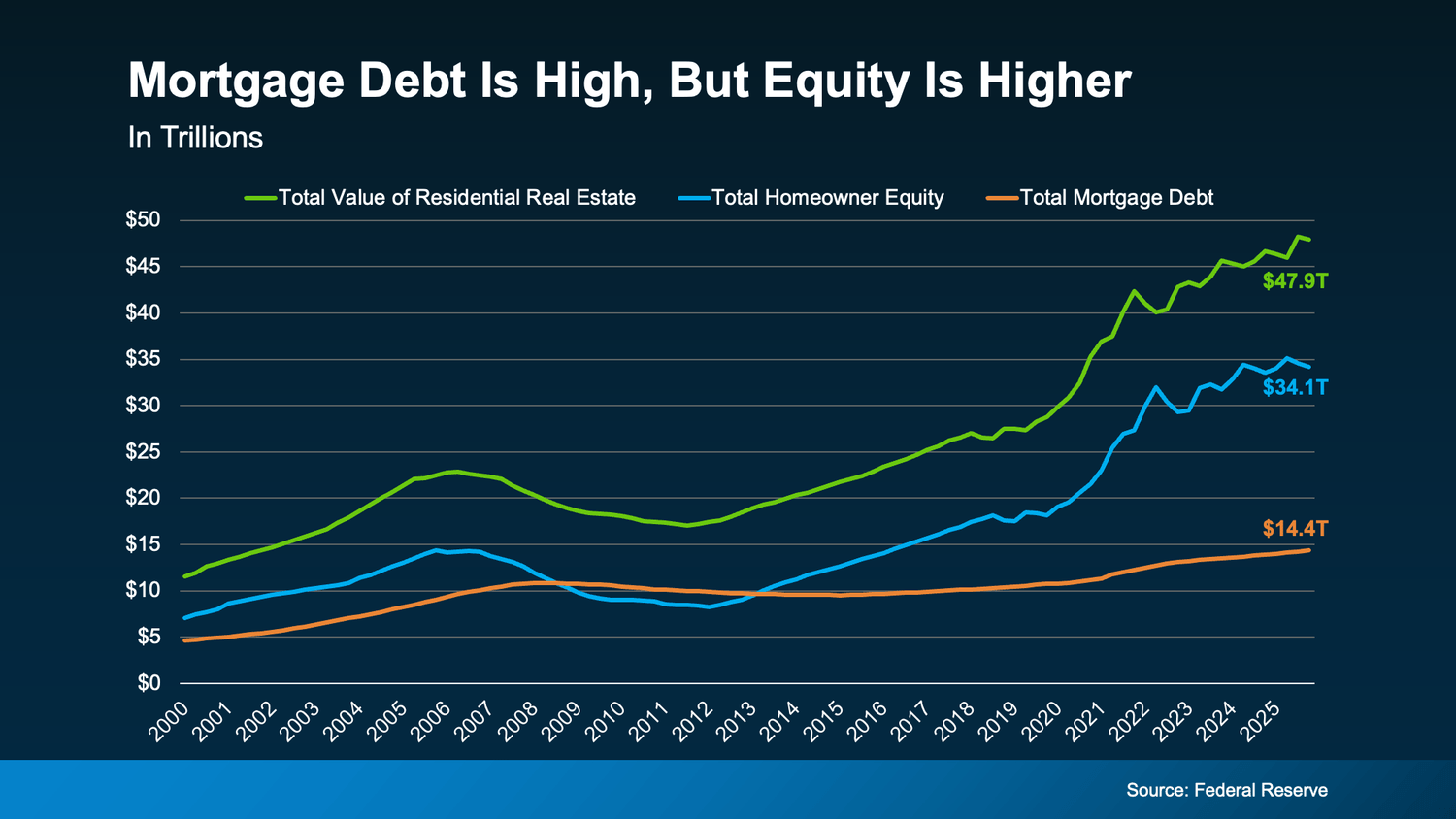

According to the Federal Reserve, total mortgage debt in the United States currently sits at about $14.4 trillion — an all-time high. Heard on its own, that sounds alarming. Especially when you're also seeing headlines about people struggling with the cost of living.

But let's look at the full picture:

Here's what that chart is actually showing you:

Total value of all U.S. homes: $47.9 trillion

Total homeowner equity: $34.1 trillion

Total mortgage debt: $14.4 trillion

Yes, debt is at a record high. But equity — what homeowners actually own — is more than double that debt number. And it's also near a record high.

Now look at the years between 2008 and 2013 on that chart. See where the orange line rises above the blue one? That's the period when the housing market was in genuine crisis. When debt exceeds equity, homeowners have no cushion. When prices fell in 2008, millions of people owed more than their homes were worth. They had no options. That's what a real housing crisis looks like.

That is not what's happening today. Today it's the exact opposite — the gap between what homeowners owe and what they own has never been wider. In a good way.

What This Looks Like at the Individual Homeowner Level

National numbers are useful for context. But what does this actually mean for the average homeowner?

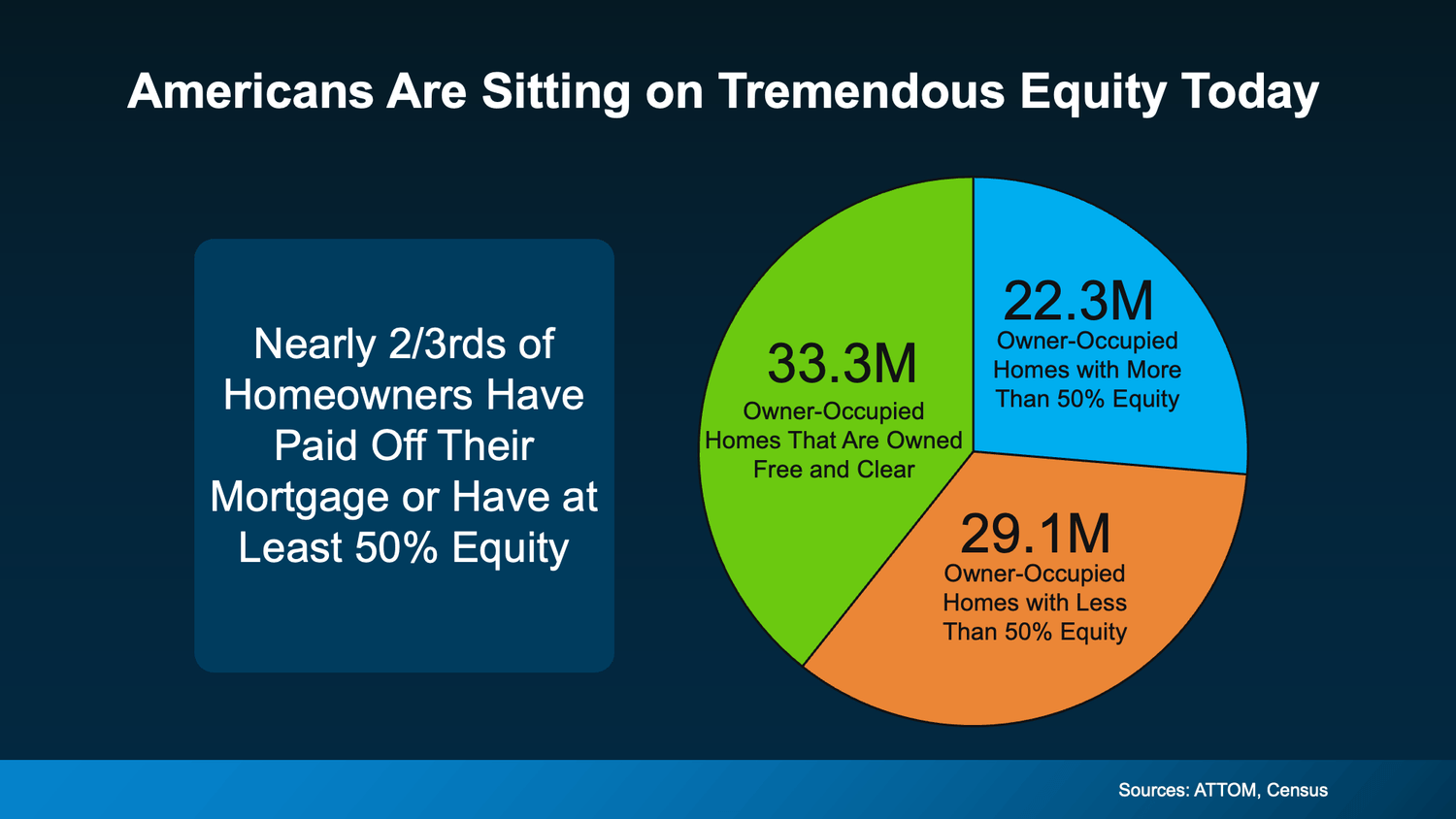

Here's what that data shows:

33.3 million homeowners own their homes completely free and clear — no mortgage, no lender, zero foreclosure risk

22.3 million homeowners have more than 50% equity in their homes — an extremely strong financial cushion

29.1 million homeowners have less than 50% equity — and most of them are simply newer buyers building equity over time in a perfectly normal way

Add the first two groups together and you're looking at nearly two-thirds of all homeowners who are either fully paid off or sitting on massive equity positions. That's not a market on the edge. That's a market built on an unusually strong foundation.

Why This Matters for Southern California Specifically

In Pasadena and LA County, long-term homeowners have seen some of the most significant equity accumulation in the country. Values have appreciated dramatically over the past decade — which means the homeowners in those markets aren't just stable, they're sitting on financial positions that would have seemed unimaginable when they first bought.

In Rancho Cucamonga and the Inland Empire, buyers who purchased even five or six years ago have built substantial equity through a combination of price appreciation and consistent mortgage payments. That equity is a buffer — against life changes, against market fluctuations, against the kind of vulnerability that made 2008 so devastating for so many families.

The structural difference between now and 2008 isn't just national — it's playing out in our own backyard.

So Why Do These Headlines Keep Getting Written?

Because big numbers generate clicks. $14 trillion sounds alarming in a headline. But $14 trillion in debt against $47.9 trillion in home value and $34.1 trillion in equity tells a completely different story — one that doesn't fit in a tweet.

The financial media's job is to get your attention. Your job is to make sound decisions about one of the largest financial assets you'll ever own. Those two things don't always point in the same direction.

That's exactly why having someone in your corner who can separate the noise from the reality matters — whether you're thinking about buying, selling, or just trying to understand what's going on in the market.

Bold LA Key Takeaway

Record mortgage debt makes for a scary headline. But when you see it next to record home values and record homeowner equity — with debt representing less than a third of total home value nationally — the story changes completely.

The conditions that created the 2008 crisis simply don't exist right now. Homeowners are on stronger footing than they've been in decades. And that's the context your brother-in-law is missing.

If you want to understand what any of this means for your specific situation — whether you're buying, selling, or just trying to make sense of the market — reach out. I'll give you straight answers, no spin.

That wraps up today's blog — appreciate you stopping by. And as always, if you want it to sell, call Terrell… and if you want to buy, I'm still the guy.

Terrell Bolden

REALTOR®

DRE#02110062

Realty Connection Group

Los Angeles, California

(323) 471-5295

Terrell Bolden has always had a passion for real estate and how it can be used as a tool to enhance daily life.

-A safe place to call home and raise a family.

-An appreciating asset that can be passed to loved ones, or used to finance the vacation of your dreams.

Terrell understands that real estate opportunities are plentiful and is deeply committed to helping others achieve their real estate dreams throughout the greater Los Angeles area.

Disclaimer: The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. Terrell Bolden, Realty Connection Group, DRE #02110062 does not guarantee or warrant the accuracy or completeness of the information or opinions contained herein. Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision. Terrell Bolden, Realty Connection Group, DRE #02110062 will not be liable for any loss or damage caused by your reliance on the information or opinions contained herein.

Let us know what you think in the comments!

Quick links

Newsletter

Subscribe to the newsletter and stay in the loop! By joining, you acknowledge that you'll receive our newsletter and can opt-out anytime hassle-free.