Renting vs. Buying: The Numbers Might Surprise You

Renting feels manageable — until it doesn't.

No down payment. No surprise repairs. No long-term commitment.

Those are real advantages, and I'm not going to pretend otherwise.

But then your rent goes up $200 a month. And then it goes up again the year after that. And somewhere along the way, the option that felt flexible starts feeling like a trap — especially when you realize you have nothing to show for the thousands of dollars you've spent on someone else's mortgage.

Here's what most people don't hear enough: the math on buying may be working better in your favor right now than you think.

In Most of the Country, Buying Is Actually Cheaper Than Renting

This one surprises people — but the data backs it up.

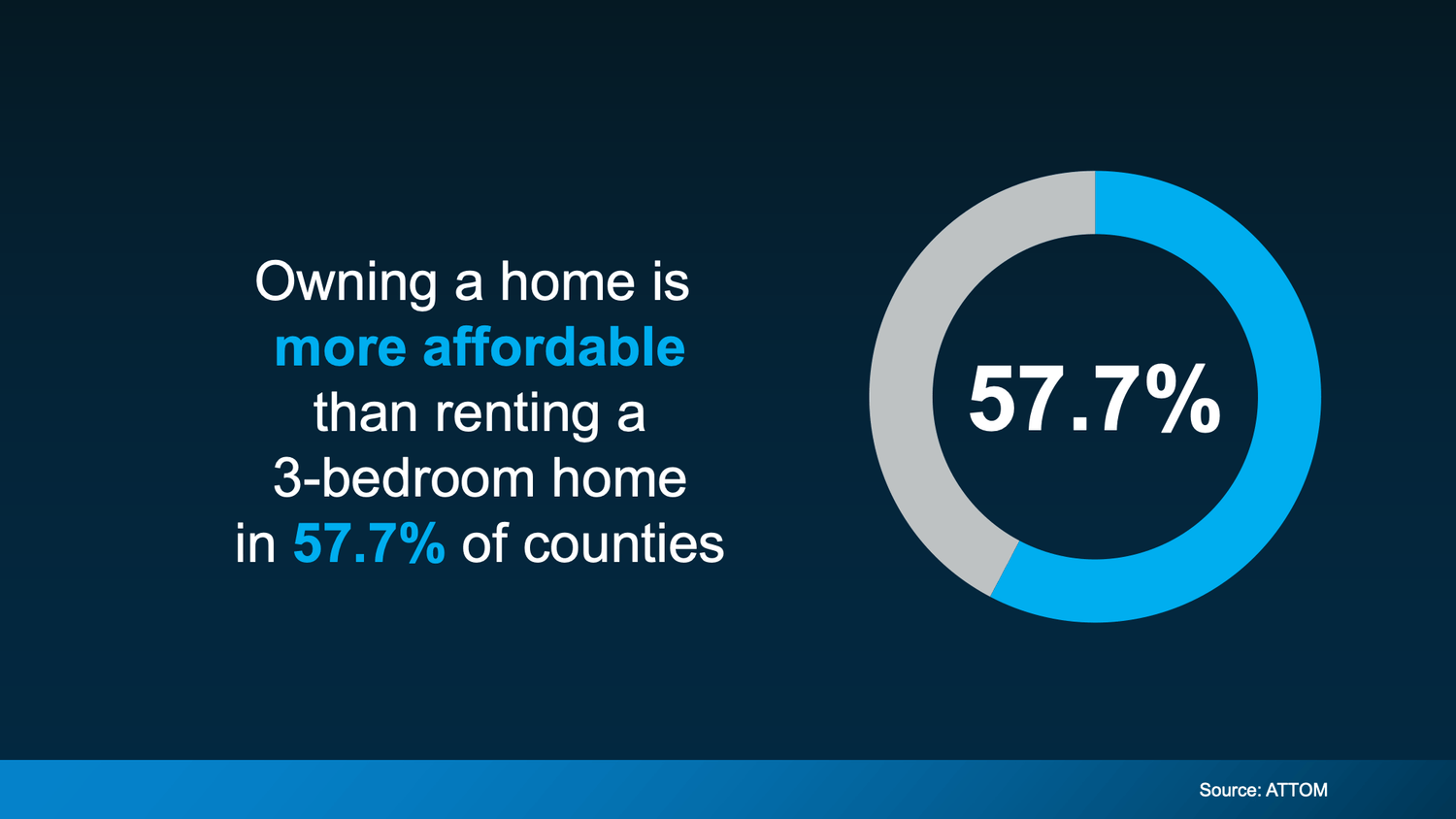

According to ATTOM, owning a home costs less per month than renting a comparable 3-bedroom home in nearly 58% of counties across the U.S. — and that's after factoring in insurance and typical maintenance costs.

Read that again. In the majority of counties in this country, the monthly cost of owning is lower than the monthly cost of renting.

Why? A combination of factors has shifted the math: home price growth has slowed, more inventory has given buyers more options, and mortgage payments have started to ease as rates have come down from their peak. The rent vs. buy equation that felt completely one-sided two or three years ago is looking different now.

But What About Southern California?

Fair question — and I'm going to be straight with you, because this is where the regional breakdown matters.

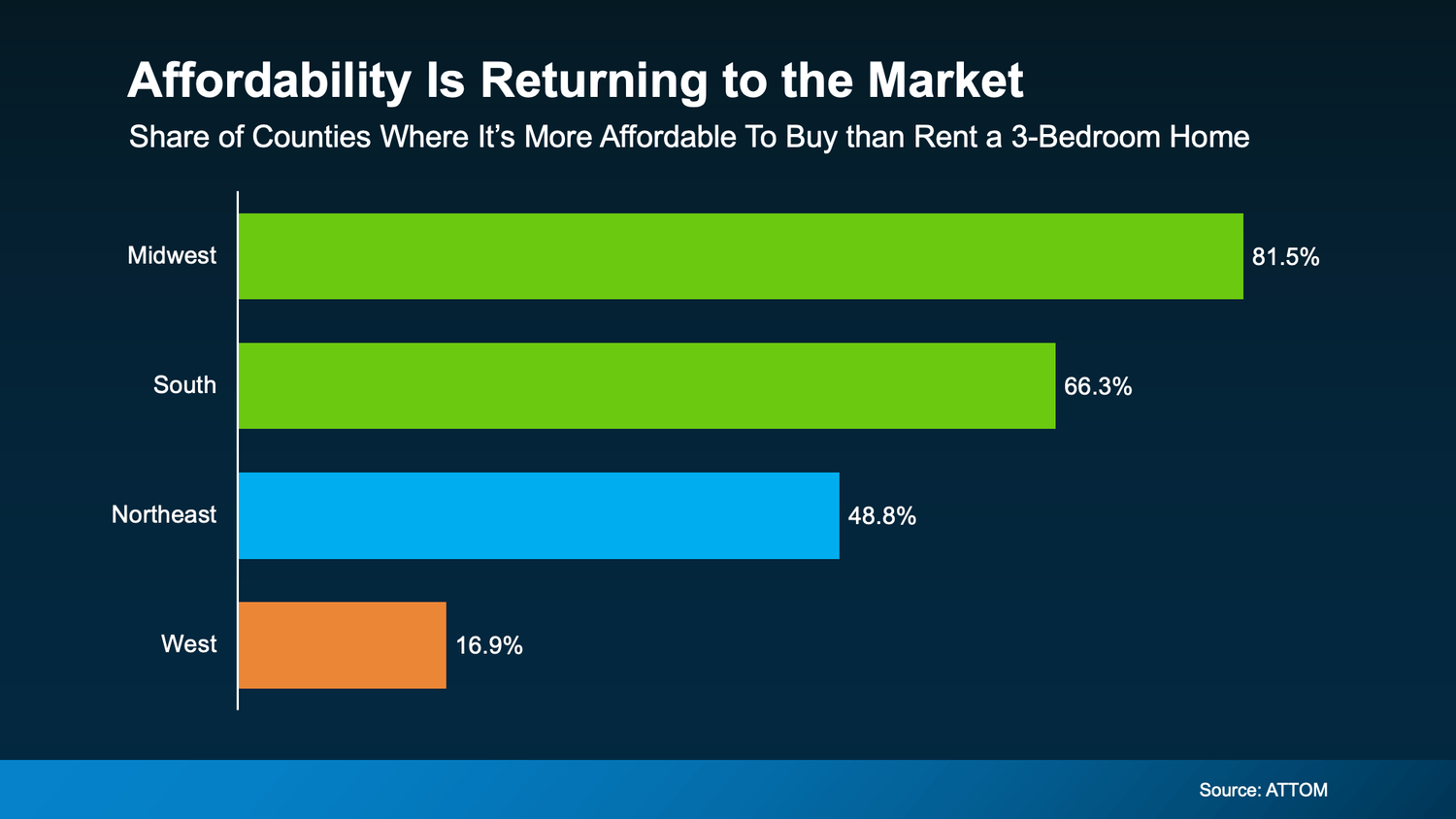

The biggest affordability improvements are happening in the Midwest and South. The West — including Southern California — is still a tighter market. Buying here isn't cheap, and pretending otherwise wouldn't be honest.

But here's the nuance that gets missed: "more expensive to buy" and "not worth buying" are two completely different things.

In Rancho Cucamonga, a buyer who purchases today is locking in a fixed monthly payment. Their neighbor who keeps renting is subject to annual rent increases with no ceiling and no equity being built. Over five or ten years, that gap compounds — and it almost always swings in the homeowner's favor.

In Pasadena, yes, the entry price is higher. But the long-term appreciation in that market has been consistent precisely because demand doesn't go away. The buyers who stretched to get in five years ago are sitting on significant equity today.

The only way to know how the numbers actually work for your situation in your target area is to look at them specifically — not rely on a national headline or a regional average.

The Real Barrier: It's Not the Monthly Payment

Here's what I hear most often from renters who've run the numbers and still feel stuck:

"Okay, but I can't afford the down payment."

And that's a legitimate concern — especially in Southern California where purchase prices are higher than the national average.

But here's the part most people never hear about: there are thousands of down payment assistance programs available across the country, and a significant number of buyers qualify without ever knowing it.

The average benefit from these programs? Around $18,000.

That's not a small number. That kind of assistance can cover a meaningful portion of your down payment or closing costs — which means the gap between where you are right now and where you need to be to buy might be considerably smaller than you assumed.

California specifically has several active programs for first-time buyers. If you haven't looked into what's available in LA County or the Inland Empire, that conversation alone could change your timeline significantly.

The Real Cost of Waiting

Let me put this in terms that are easy to visualize.

If you're paying $2,500 a month in rent right now, that's $30,000 a year going toward someone else's investment. Over five years, that's $150,000 — and that assumes your rent never goes up, which we both know isn't realistic.

Meanwhile, a homeowner making the same monthly payment is building equity, benefiting from any appreciation in their home's value, and locking in a payment that doesn't change year over year.

The gap between those two paths doesn't stay the same over time. It widens — consistently, in favor of the homeowner.

This Isn't About Rushing Into Anything

I want to be clear about something: the point here isn't that everyone should go buy a home tomorrow. Buying only makes sense when the timing is right for your specific situation — your income, your savings, your stability, your goals.

But what I don't want is for you to stay stuck in the "someday" loop based on assumptions that may no longer be accurate. Because the belief that renting is always the more affordable option? For a lot of people in a lot of markets, the data simply doesn't support that anymore.

Bold LA Key Takeaway

Renting isn't automatically the safe financial choice — and buying isn't automatically out of reach. The real answer lives in your specific numbers, in your specific market, with your specific financial picture.

If you've been telling yourself that homeownership is a someday thing, let's actually look at what someday could mean for you right now. You might be closer than you think — and the cost of waiting might be higher than you realize.

Let's run the numbers together. No pressure, just clarity on what's actually possible for your situation.

Terrell Bolden

REALTOR®

DRE#02110062

Realty Connection Group

Los Angeles, California

(323) 471-5295

Terrell Bolden has always had a passion for real estate and how it can be used as a tool to enhance daily life.

-A safe place to call home and raise a family.

-An appreciating asset that can be passed to loved ones, or used to finance the vacation of your dreams.

Terrell understands that real estate opportunities are plentiful and is deeply committed to helping others achieve their real estate dreams throughout the greater Los Angeles area.

Disclaimer: The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. Terrell Bolden, Realty Connection Group, DRE #02110062 does not guarantee or warrant the accuracy or completeness of the information or opinions contained herein. Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision. Terrell Bolden, Realty Connection Group, DRE #02110062 will not be liable for any loss or damage caused by your reliance on the information or opinions contained herein.

Let us know what you think in the comments!

Quick links

Newsletter

Subscribe to the newsletter and stay in the loop! By joining, you acknowledge that you'll receive our newsletter and can opt-out anytime hassle-free.