The 20% Down Payment Rule Is a Myth. Here's What First-Time Buyers Are Actually Putting Down.

One of the most common reasons first-time buyers put their home search on hold is the belief that they need to save up 20% before they can even think about making a move.

That belief is costing people years of equity building — and it's simply not accurate.

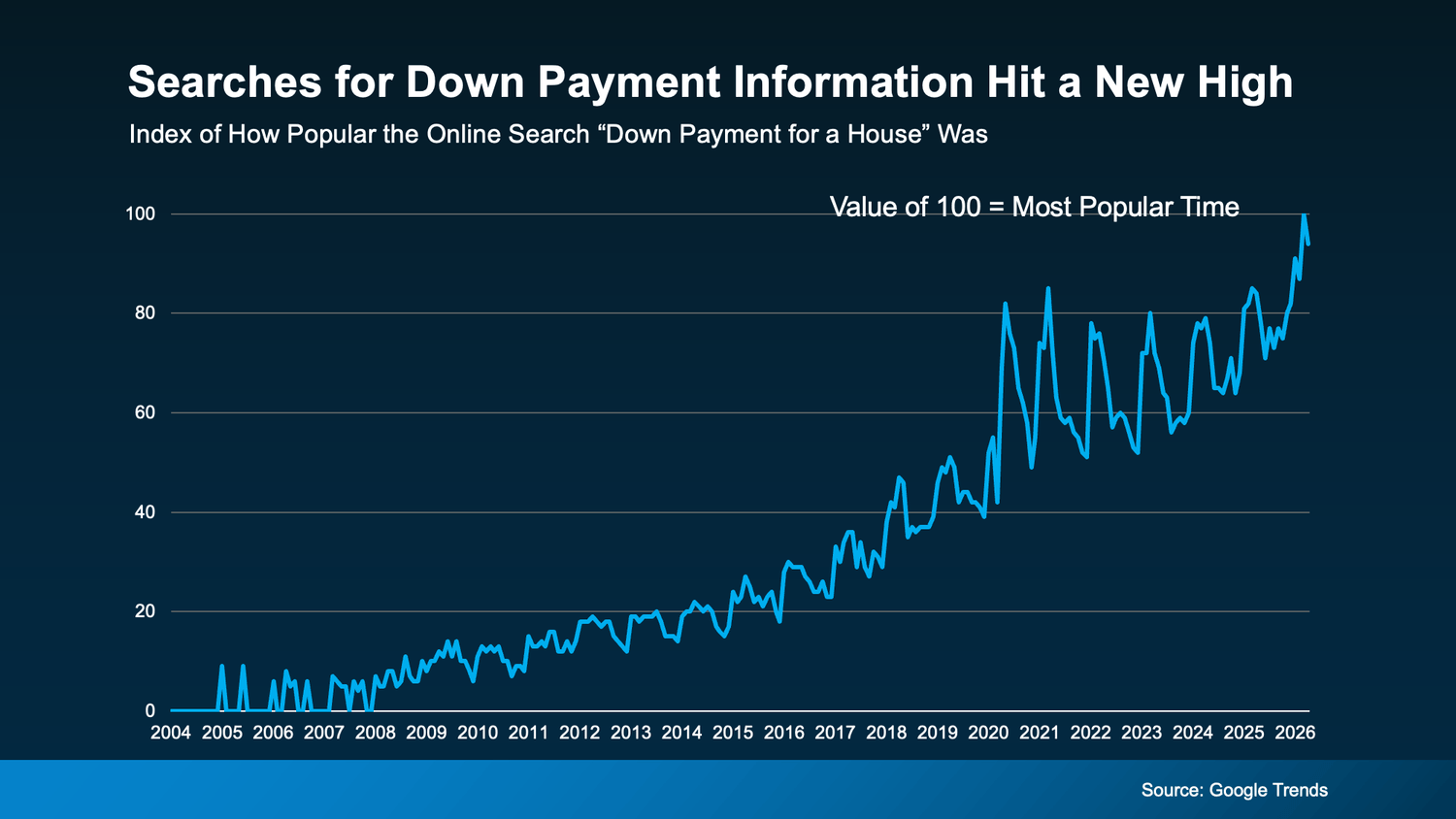

Searches for Down Payment Info Just Hit an All-Time High

According to Google Trends, online searches for down payment information recently hit an all-time high. That tells you something important: a lot of buyers are trying to figure out what they actually need — and a lot of them are probably operating on bad information.

So let's clear it up right now.

Where the 20% Myth Comes From — And Why It's Holding Buyers Back

The 20% figure isn't completely made up. Putting 20% down does have real benefits — it eliminates private mortgage insurance (PMI), lowers your monthly payment, and gives you more equity from day one.

But here's what that number was never meant to be: a requirement. And for most first-time buyers, it isn't one.

As the Mortgage Reports explains, many homebuyers are able to secure a home with as little as 3% — or even no down payment at all — depending on the loan type and their financial situation.

Here's a quick breakdown of what's actually available:

FHA loans — down payments as low as 3.5%

Conventional loans — some options as low as 3% for qualifying buyers

VA loans — zero down for eligible veterans and active military

USDA loans — zero down for qualifying buyers in eligible areas

For first-time buyers in Rancho Cucamonga and the Inland Empire, FHA loans in particular have been a popular path — they're accessible, flexible on credit requirements, and allow buyers to get into a home without draining their savings entirely. For veterans across LA County and the Inland Empire, a VA loan is one of the most powerful financial tools available — and far too many eligible buyers don't know they qualify.

What Buyers Are Actually Putting Down

So if 20% isn't the norm, what are first-time buyers actually doing?

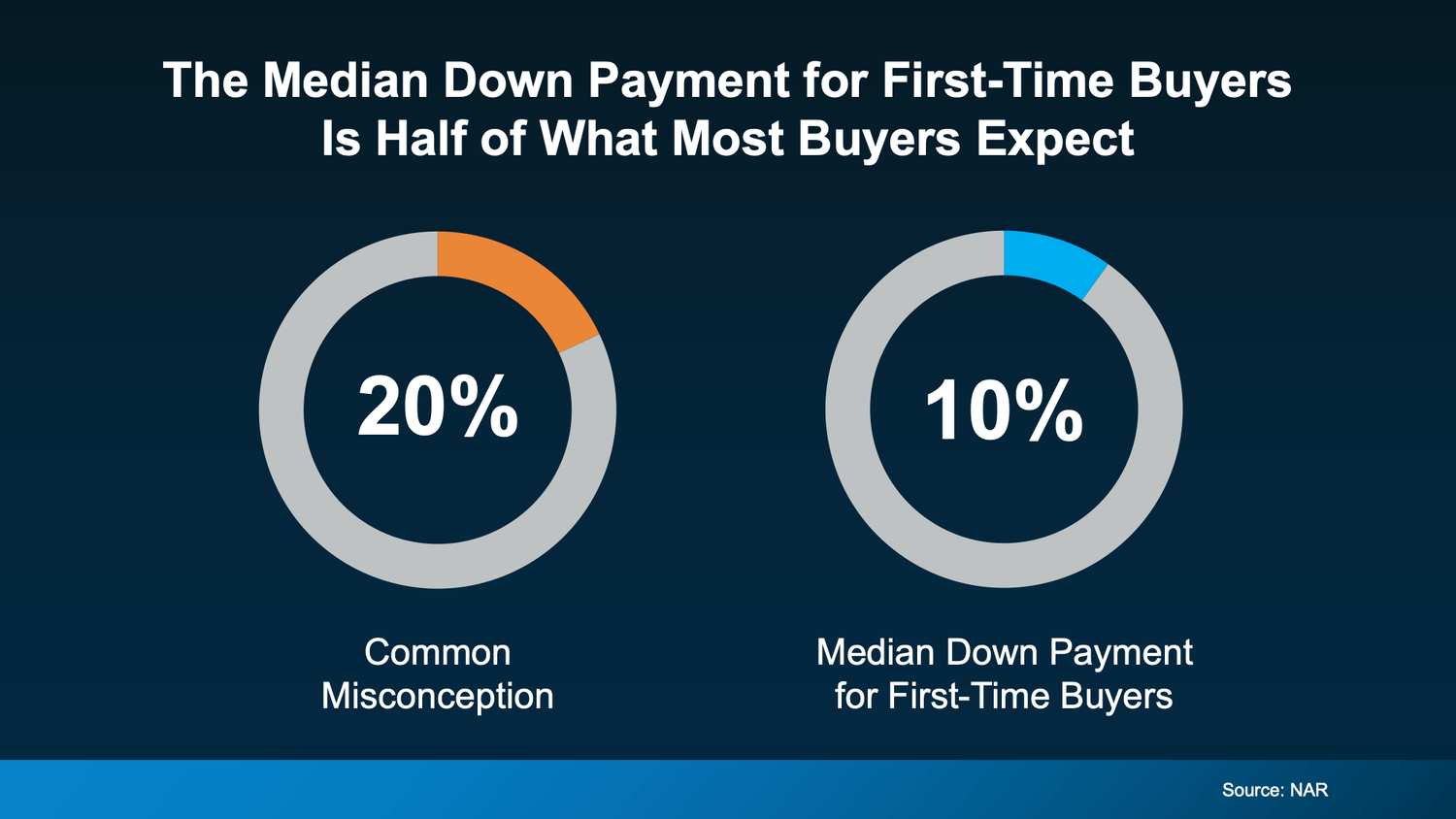

According to the National Association of Realtors, the median down payment for first-time homebuyers is 10% — exactly half of what most people assume they need.

Read that again. The typical first-time buyer is putting down 10% — not 20%. And plenty are putting down even less than that using the loan programs mentioned above.

If you've been building a savings timeline around the 20% figure, you may be waiting significantly longer than you need to. That's not a small thing — every year you wait is a year someone else is building equity while your rent check builds nothing.

The Tool Most Buyers Don't Know Exists — But Should

Here's where it gets even more interesting. Not only do most first-time buyers not need 20% down — many of them can get significant help reaching whatever down payment they do need.

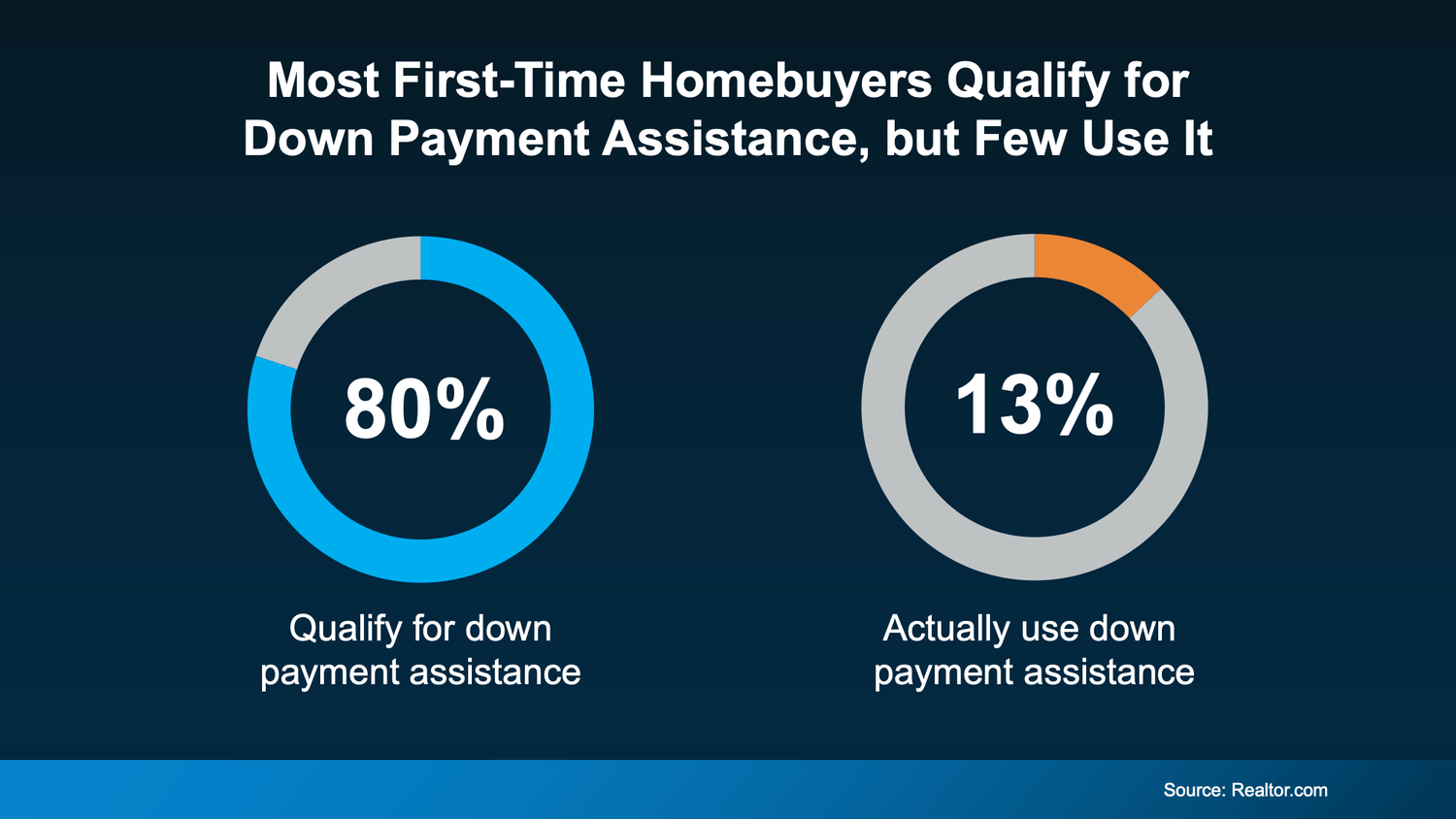

Research from Realtor.com shows that nearly 80% of first-time homebuyers qualify for down payment assistance (DPA). But only 13% actually use it.

That gap is enormous — and it represents tens of thousands of buyers leaving money on the table simply because they didn't know it existed or assumed they wouldn't qualify.

There are currently over 2,600 homeownership assistance programs available across the country. According to Down Payment Resource, the average benefit is around $18,000 — and in some cases, buyers can stack multiple programs to boost their savings even further.

Think about what an extra $18,000 does for a first-time buyer in Southern California. On an FHA loan with a 3.5% down payment on a $550,000 home, that assistance could cover the entire down payment and a significant portion of closing costs. That's the difference between buying this year and waiting two or three more years.

California has several active programs worth knowing about — and a good lender who knows the local landscape can tell you quickly which ones you might qualify for.

The Conversation Worth Having Right Now

Here's the bottom line: if you've been sitting on the sidelines because you don't have 20% saved, you may already have everything you need to buy — you just don't know it yet.

The first step isn't saving more money. It's having a real conversation with a trusted lender who can tell you exactly what your options are based on your actual financial picture. That conversation costs you nothing. And it might tell you that you're a lot closer to buying than you thought.

Bold LA Key Takeaway

The 20% down payment myth is one of the most expensive misconceptions in real estate — because it keeps ready buyers on the sidelines for years longer than necessary.

Most first-time buyers put down 10% or less. Loan programs exist for as little as 3.5% down. And nearly 80% of first-time buyers qualify for assistance they're not using.

If you want to know what buying actually looks like for your situation right now — what you need, what you qualify for, and how close you really are — let's talk. I'll connect you with the right people and help you understand your real options.

That wraps up today's blog — appreciate you stopping by. And as always, if you want it to sell, call Terrell… and if you want to buy, I'm still the guy.

Terrell Bolden

REALTOR®

DRE#02110062

Realty Connection Group

Los Angeles, California

(323) 471-5295

Terrell Bolden has always had a passion for real estate and how it can be used as a tool to enhance daily life.

-A safe place to call home and raise a family.

-An appreciating asset that can be passed to loved ones, or used to finance the vacation of your dreams.

Terrell understands that real estate opportunities are plentiful and is deeply committed to helping others achieve their real estate dreams throughout the greater Los Angeles area.

Disclaimer: The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. Terrell Bolden, Realty Connection Group, DRE #02110062 does not guarantee or warrant the accuracy or completeness of the information or opinions contained herein. Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision. Terrell Bolden, Realty Connection Group, DRE #02110062 will not be liable for any loss or damage caused by your reliance on the information or opinions contained herein.

Let us know what you think in the comments!

Quick links

Newsletter

Subscribe to the newsletter and stay in the loop! By joining, you acknowledge that you'll receive our newsletter and can opt-out anytime hassle-free.