Adjustable-Rate Mortgages Are Back in the Conversation. Here's What That Actually Means for You.

If you've been house hunting lately and feeling the squeeze on affordability, you're not alone. And you're probably starting to hear a term come up more often — adjustable-rate mortgage, or ARM.

So let's talk about it honestly. What is it, why are more buyers using it, and is it something you should even consider?

First, Let's Break Down What an ARM Actually Is

Most people are familiar with a fixed-rate mortgage — your rate stays the same for the life of the loan, your payment stays predictable, end of story.

An ARM works differently. You get a fixed rate for an initial period — usually 5, 7, or 10 years — and after that, the rate adjusts periodically based on market conditions. If rates have gone up by then, your payment goes up. If they've gone down, your payment drops.

Here's the simple version:

Fixed-rate: Predictable. Same payment for 30 years.

Adjustable-rate: Lower to start. Could change later.

That's the core tradeoff. Lower payment now, some uncertainty later.

Why Buyers Are Paying Attention to ARMs Right Now

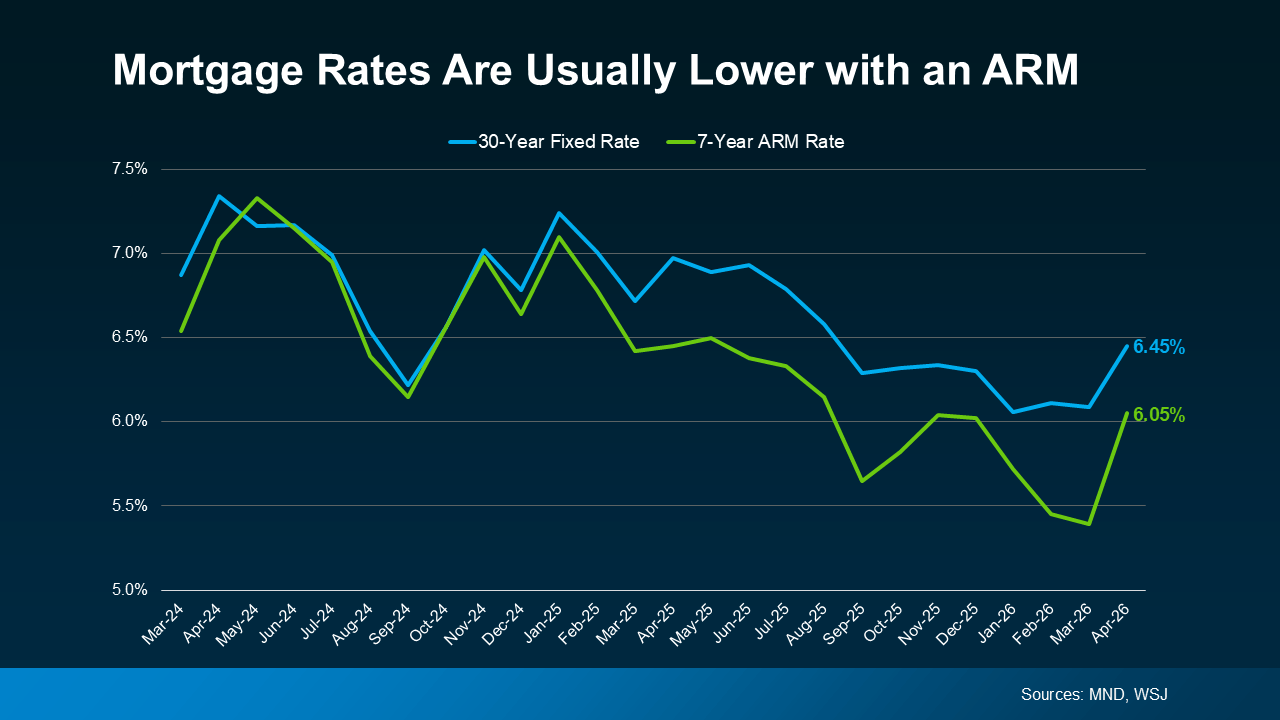

The reason ARMs are getting more attention comes down to one thing — the upfront rate is lower than a 30-year fixed mortgage. And right now, that difference is real enough to matter.

According to Redfin, the typical buyer could save around $150 per month by choosing an ARM over a 30-year fixed right now. For a first-time buyer in Rancho Cucamonga trying to make the numbers work on a $500,000–$600,000 home, that's not a small thing. That's $1,800 a year back in your pocket during the years you probably need it most.

More Buyers Are Making This Choice

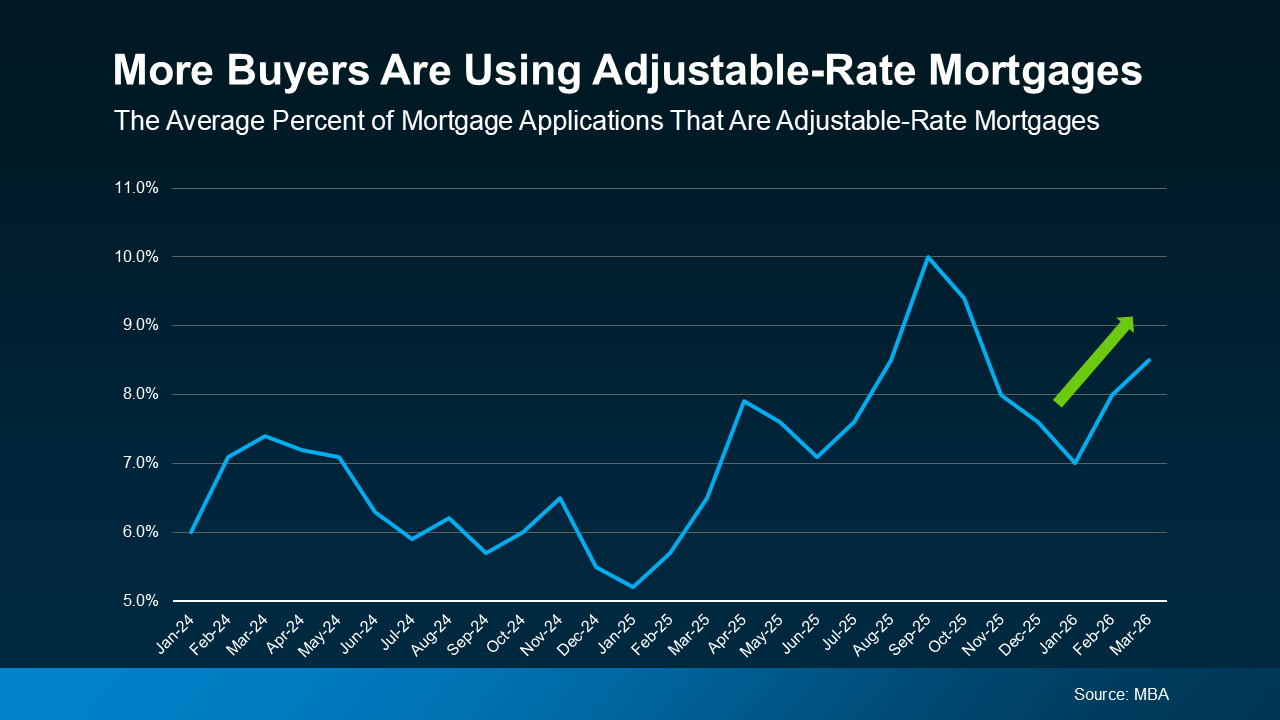

It's not just a few people doing this. Data from the Mortgage Bankers Association shows the share of buyers choosing ARMs has been climbing — particularly as affordability has tightened over the last few years.

And before that triggers any flashbacks to 2008 — let's address that directly.

Today's ARMs are not the same products that contributed to the housing crash. Back then, lenders were approving buyers for loans they couldn't realistically afford once rates adjusted. Those guardrails didn't exist.

Today, lending standards are significantly stricter. Lenders actually evaluate whether you could handle the payment if rates were to rise before approving you. The return of ARMs isn't a warning sign — it's buyers being creative and strategic in a tough affordability environment.

So Is an ARM Right for You? Here's How to Think About It.

This is where I'd sit down with a client and walk through their specific situation — because the honest answer is, it depends.

An ARM could make sense if:

You're planning to sell or move within 5–7 years before the rate ever adjusts. In that case, you get all the savings upfront with none of the uncertainty later.

You're early in your career and confident your income will grow meaningfully over the next several years — giving you more flexibility when the rate does adjust.

You're buying in a market like Pasadena where you plan to hold the property long-term but expect to refinance once rates come down.

An ARM may not be the right fit if:

You need the certainty of a fixed payment for budgeting purposes.

You're planning to stay in the home long-term and rates don't come down the way you're hoping.

The idea of your payment potentially increasing keeps you up at night — that's a real factor worth respecting.

Here's the part most people skip over: there's no guarantee rates will drop in time for you to refinance your way out of an ARM. That's a plan, not a guarantee. And you need to go in with eyes wide open about that.

The Bigger Picture for SoCal Buyers

In Southern California, where entry-level prices in desirable areas can still push $550,000–$700,000+, buyers are looking for every legitimate tool available to make ownership work. ARMs are one of those tools — not a shortcut, not a risk to take blindly, but a real option worth understanding.

The buyers I work with in Rancho Cucamonga and Pasadena who've used ARMs strategically did so with a clear plan — they knew their timeline, they ran the numbers on both scenarios, and they made an informed decision. That's the difference between a smart financial move and a gamble.

Bold LA Key Takeaway

ARMs are getting attention again because they work for certain buyers in certain situations — and right now, that group is growing. But "certain situations" is the key phrase.

Before you go down this road, you need to understand exactly how the loan works, what happens when the fixed period ends, and whether your plan holds up even if rates don't move the way you're hoping.

That's not a conversation to have with Google. That's a conversation to have with a trusted lender — and an agent who can help you think through the full picture.

If you want to talk through whether an ARM makes sense for your situation, let's connect. I'll help you ask the right questions before you make any decisions.

Terrell Bolden

REALTOR®

DRE#02110062

Realty Connection Group

Los Angeles, California

(323) 471-5295

Terrell Bolden has always had a passion for real estate and how it can be used as a tool to enhance daily life.

-A safe place to call home and raise a family.

-An appreciating asset that can be passed to loved ones, or used to finance the vacation of your dreams.

Terrell understands that real estate opportunities are plentiful and is deeply committed to helping others achieve their real estate dreams throughout the greater Los Angeles area.

Disclaimer: The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. Terrell Bolden, Realty Connection Group, DRE #02110062 does not guarantee or warrant the accuracy or completeness of the information or opinions contained herein. Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision. Terrell Bolden, Realty Connection Group, DRE #02110062 will not be liable for any loss or damage caused by your reliance on the information or opinions contained herein.

Let us know what you think in the comments!

Quick links

Newsletter

Subscribe to the newsletter and stay in the loop! By joining, you acknowledge that you'll receive our newsletter and can opt-out anytime hassle-free.