Mortgage Rates Are Moving Around. Here's What You Can Actually Do About It.

Let's be real — mortgage rates have been all over the place lately. And if you're trying to plan a home purchase, that kind of uncertainty can make it feel like you're trying to hit a moving target.

But here's the mindset shift that changes everything: you can't control where rates go. You can control how prepared you are when they move.

So let's focus on what actually matters.

First, Let's Put the Volatility in Context

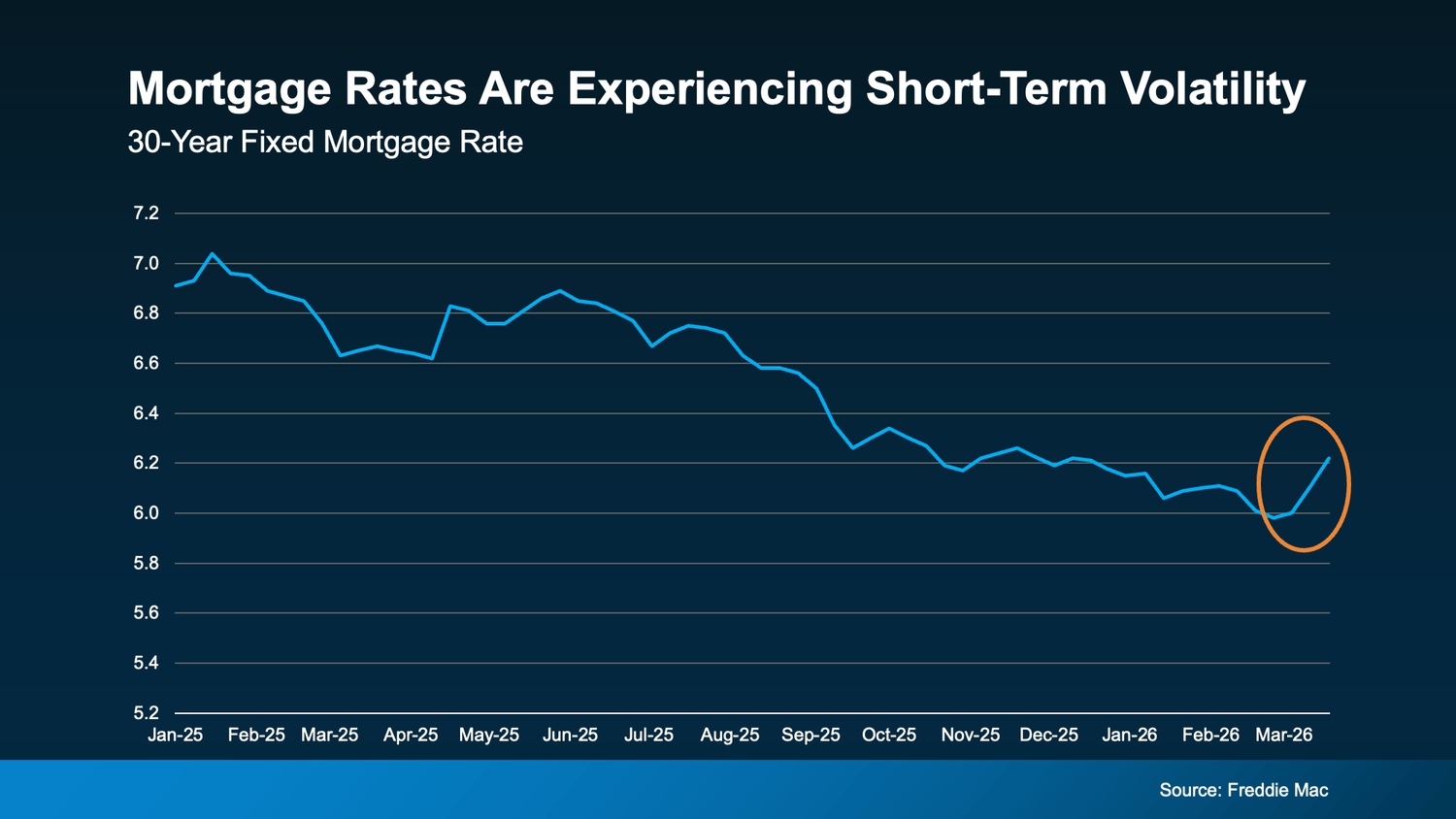

After trending downward for well over a year, rates have ticked back up over the past month. And if you've been watching closely, that probably stings a little.

But zoom out for a second. If you look at that same graph over a longer period, you'll notice something — this isn't the first time rates have bumped up mid-trend. There have been multiple moments in just the past year where rates inched higher before resuming their direction.

We're in one of those moments right now.

When there's economic uncertainty or global events shaking the financial markets, mortgage rates respond. That's not a malfunction — that's just how it works. As Investopedia explains, mortgage rates don't move in isolation, and as long as uncertainty stays elevated, some rate swings should be expected.

Knowing that doesn't make the volatility disappear. But it does mean you shouldn't be making major life decisions based on what rates did last Tuesday.

So What Can You Actually Control?

Glad you asked. Because while the broader rate environment is out of your hands, there are three things that directly affect the rate you personally qualify for — and all three are within your control.

1. Your Credit Score

This is the biggest lever most buyers aren't paying enough attention to.

Your credit score doesn't just determine whether you get approved — it determines the terms of your approval. The difference between a 680 and a 740 credit score can mean a meaningfully different interest rate on the same loan amount. And over a 30-year mortgage, that difference adds up to real money.

As Bankrate puts it, the higher your score, the lower the interest rate and the better the terms you'll typically qualify for.

If you're not sure where your credit stands right now, that's the first conversation to have with a lender. They can tell you exactly where you are and what — if anything — would make a difference before you apply.

In Southern California, where loan amounts tend to be higher than the national average, even a small rate improvement has an outsized impact on your monthly payment. This one is worth taking seriously.

2. Your Loan Type

Not all mortgages are created equal — and a lot of buyers don't realize how much the loan type itself can affect the rate they receive.

Conventional, FHA, VA, USDA — each one has different eligibility requirements, different down payment thresholds, and different rate structures. For first-time buyers in Rancho Cucamonga or anywhere in the Inland Empire, FHA loans can open doors that conventional financing doesn't. For veterans, a VA loan can be a game-changer on both rate and down payment.

The Consumer Financial Protection Bureau makes it clear — rates can be significantly different depending on which loan type you choose.

This is exactly why talking to a lender early matters. You want to know which loan types you qualify for before you fall in love with a house — not after.

3. Your Loan Term

The length of your loan affects more than just how long you're making payments. It directly impacts your interest rate and your total cost of borrowing.

A 15-year mortgage will typically come with a lower rate than a 30-year — but a higher monthly payment. A 30-year gives you more breathing room month to month but costs more in interest over time. A 20-year sits somewhere in between.

As Freddie Mac notes, your loan term affects your interest rate, your monthly payment, and the total interest you'll pay over the life of the loan. There's no universal right answer — it depends on your income, your budget, and your long-term goals.

The right lender will walk you through all three scenarios side by side so you can make an informed decision, not a guess.

The Bottom Line on Timing

Here's what I tell every buyer I work with in LA County and the Inland Empire who's stressing about rates:

Trying to time the market is a losing game. Rates could drop next month. They could stay flat. They could tick up again. Nobody knows — not the Fed, not the economists, not the financial influencers on YouTube.

What you can do is show up with a strong credit profile, the right loan type for your situation, and a clear understanding of your term options. That combination puts you in the best possible position to get a competitive rate — regardless of what the broader market is doing.

The buyers who win aren't the ones who waited for the perfect rate. They're the ones who controlled what they could and moved when the time was right for them.

Bold LA Key Takeaway

Rates are going to keep moving. That's not going to change. What can change is how prepared you are to move confidently when the right opportunity shows up.

If you want to talk through where you stand — your credit, your loan options, what a realistic monthly payment looks like at today's rates — let's connect. I'll help you focus on the controllables so you're not sitting on the sidelines waiting for a perfect moment that may never come.

Let's run the numbers and build a real plan around your situation.

Terrell Bolden

REALTOR®

DRE#02110062

Realty Connection Group

Los Angeles, California

(323) 471-5295

Terrell Bolden has always had a passion for real estate and how it can be used as a tool to enhance daily life.

-A safe place to call home and raise a family.

-An appreciating asset that can be passed to loved ones, or used to finance the vacation of your dreams.

Terrell understands that real estate opportunities are plentiful and is deeply committed to helping others achieve their real estate dreams throughout the greater Los Angeles area.

Disclaimer: The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. Terrell Bolden, Realty Connection Group, DRE #02110062 does not guarantee or warrant the accuracy or completeness of the information or opinions contained herein. Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision. Terrell Bolden, Realty Connection Group, DRE #02110062 will not be liable for any loss or damage caused by your reliance on the information or opinions contained herein.

Let us know what you think in the comments!

Quick links

Newsletter

Subscribe to the newsletter and stay in the loop! By joining, you acknowledge that you'll receive our newsletter and can opt-out anytime hassle-free.